Elsewhere, fintech is solving problems Silicon Valley never had

How do you launch successful fintech companies when the infrastructure isn’t there? Elsewhere founders are building it themselves.

In 2021, Puerto Rican founders Farooq Malik and Charles Yoo-Naut had a thesis that financial infrastructure around the world needed an upgrade — and new ideas.

“If you’re in an emerging market, you can’t just walk into the bank and open up a US-dollar bank account,” Charles said. “But you can get access to stablecoins.”

They saw that stablecoins — a type of cryptocurrency backed by traditional assets like the US dollar — could help make remittances, cross border payment, contractor payments much easier by acting as a substitute for access to dollar accounts. To embrace that opportunity, Farooq and Charles founded Rain, a global fintech infrastructure company, which enables businesses to offer stablecoin-backed credit cards.

“There’s an opportunity to move from electronic money… to digital money,” explained Farooq. “It’s the difference between a fax and an email.” Rain, which has just hit a $1.95B valuation, may be based in New York but 70% of their clients are in Latin America, drawn to stablecoin-based products as a solution for challenges like currency volatility and a widespread distrust in traditional banking. Emerging markets are driving global stablecoin adoption, which has grown 40% year-over-year in Latin America and Africa, compared to just 4% in North America.

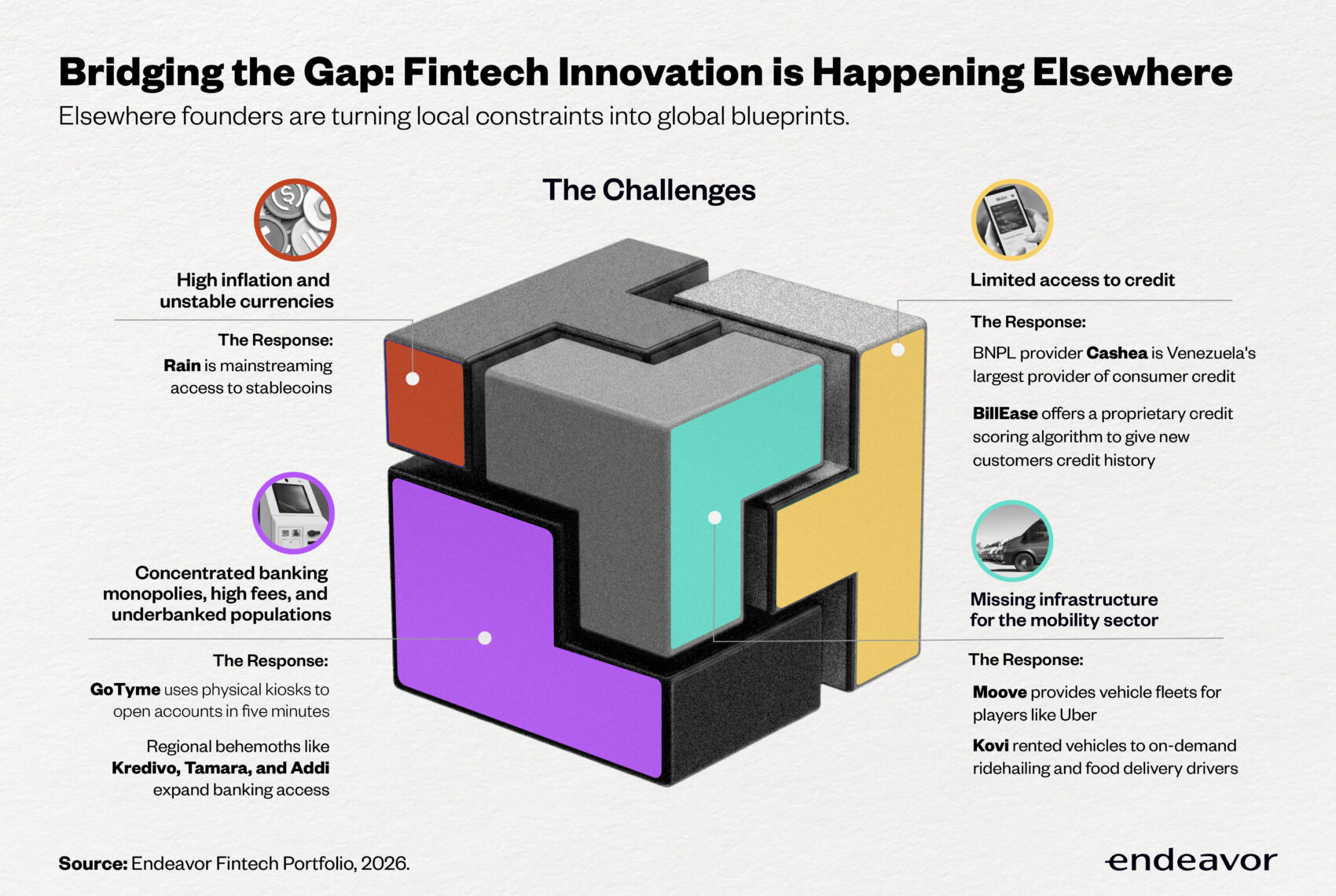

Stablecoins are only one of these breakthroughs. Across emerging markets, founders are solving problems Silicon Valley rarely had to confront: limited access to dollar-denominated banking, concentrated banking monopolies, missing credit infrastructure, or entire industries blocked by lack of financing. What begins as a workaround for local constraints often evolves into a global blueprint, fuelling innovation.

Bypassing banking fees

Farooq and Charles were speaking at an investor gathering in New York in December 2025 for Endeavor Catalyst, our venture capital fund backing companies by Endeavor Entrepreneurs, which has backed many transformative fintech companies across the world.

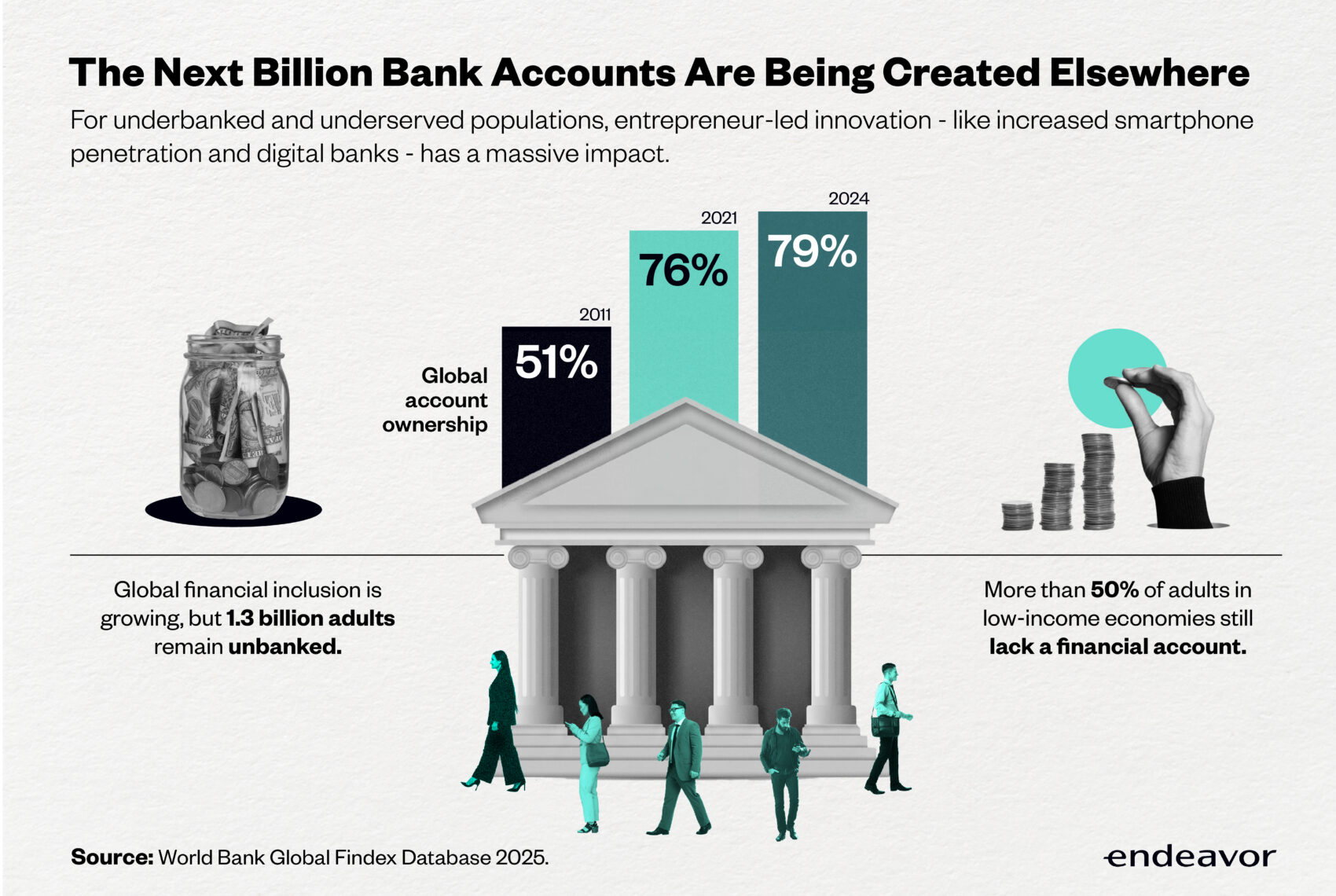

In Brazil, we backed Neon, Stark Bank, and Cora and, in Mexico, Klar — a few of the digital banks that formed as part of the same wave as Nubank, which launched in 2013 back when five banks controlled 80% of Brazil’s market and now trades publicly on the New York Stock Exchange with a $90B valuation and more than 120 million customers across Latin America.

Similarly, back in 2019, four legacy banks dominated South Africa, holding 90% of the country’s financial assets. And in the Philippines, nearly half of Filipino adults still don’t have a formal bank account.

South Africa’s GoTyme (once known as Tyme Group) used physical kiosks to help users open accounts in under five minutes. They’ve since become a unicorn (thanks in part to investment from Nubank themselves), been named one of TIME’s 100 most influential companies of 2025, and acquired 17 million customers across a growing portfolio of regions — including the Philippines.

And it’s in the Philippines that we’re likely to see this next stage of access unfold. A growing middle class, increased smartphone penetration, and regulatory tailwinds are leading the country toward greater financial inclusion, driven in large part by the explosion of digital banking options.

Some of these options, like GoTyme, are Elsewhere-to-Elsewhere, companies that have recognized issues from across the globe as akin to their own local problems and expanded consequently. Others, like Tonik or BillEase, are home-grown: led by Endeavor Entrepreneur Greg Krasnov, Tonik is the first digital-only neobank in the Philippines and recently highlighted a path to profitability for 2026, while Endeavor Entrepreneurs Georg Steiger, Ritche Weekun, and Huyen Nguyen at BillEase offer a proprietary credit scoring algorithm to provide unbanked customers with a credit history.

In the US and Europe, digital banks tend to be single-to-few product companies, like Chime and Revolut. But in Elsewhere regions suffering from high bank fees, poor customer service, and an underbanked population, they can transform daily living entirely. These companies have higher ambitions, offering multiple products as challenges to traditional banks and aspiring to become full-stack fintech platforms.

Providing credit alternatives

Venezuelan app Cashea launched in 2022 to a dramatic silence. No downloads, no transactions. Co-Founders Pedro Vallenilla, Ramón Lange, Nicolás Curat and Arnoldo Gabaldón were shocked: they’d thought offering interest-free buy-now, pay-later (BNPL) services in a country with no credit options would be an instant success.

Then they realized their problem: they’d been expecting an online customer base, when most of their customers were offline. They pivoted to deploying in-store ambassadors to onboard customers and merchants, and the results have been equally dramatic. Cashea is now the largest provider of consumer credit in Venezuela and the biggest BNPL player in Latin America, processing $100M transactions to date. “Cashear”, meaning to use Cashea’s financing product, has become an everyday Venezuelan neologism.

BNPL apps are useful tools globally, but in countries which lack access to credit or where a widespread lack of banking means that many customers don’t have credit scores, they offer a life raft for self-financing and flexibility.

Venezuela is known for its volatile economy, but it’s far from the only Elsewhere region where a local population is hungry for such tools. In Southeast Asia, Indonesian fintech Kredivo is expanding its instant credit offering, with a recent acquisition of Vietnamese digital bank Timo. Tabby was the first company to offer BNPL services across the Gulf countries, while the Saudi BNPL unicorn Tamara is a regional behemoth. In Mexico, Kueski offers financial services for customers ineligible for traditional banking, while Colombian fintech Addi has become the country’s go-to way to pay, shop, and bank, and was named this year to a Financial Times list of the fastest-growing companies in the Americas.

Powering mobility markets

The ridesharing industry owes its success in the US and other Western countries to the fact that most people own a car or have access to financing that can help them buy a car. But what happens to the industry in regions which lack car access or an accessible credit system?

For companies like Moove in Nigeria and Kovi in Brazil, the answer was clear: you build the infrastructure that props up the rideshare industry.

Co-Founder and CEO Ladi Delano launched Moove when he realized that Uber was struggling in Nigeria because of a lack of quality vehicle supply. Moove bought a fleet of vehicles for Uber’s exclusive use, on two conditions: Uber referred all drivers who needed a vehicle to Moove, and Uber offered Moove financial domiciliation, paying driver earnings directly to Moove and offering the company the chance to collect fees before remitting the rest to the driver. This model eliminated customer acquisition costs and greatly reduced collection risk, which meant that Moove could offer a wide new base of drivers in Nigeria affordable and favorable payment terms.

After Moove’s local success, Ladi expanded the company’s reach to Africa, the Middle East, Europe, and Asia, with its most recent launch in India. Today, Moove has facilitated more than 120 million trips on ride-hailing platforms across 18 cities and 11 countries. In its global tour, another Endeavor company caught Ladi’s eye: Kovi.

Kovi Co-Founders Joao Costa and Adhemar Milani Neto met when they were both executives at 99, a ridehailing app giant that became Brazil’s first tech unicorn. 99 was a success story, but Joao and Adhemar realized that a large proportion of Brazil’s population were shut out of that success because they couldn’t buy a car. They created Kovi to expand access into the industry, renting vehicles to on-demand drivers working for both ridehailing and food delivery companies.

And in 2025, Kovi was acquired by Moove: a moment where all the synergies and potential in two diverse Elsewhere markets became clear.

From local workaround to global blueprint

Stablecoins built to survive inflation become global payment infrastructure. Digital banks created to dodge predatory fees become blueprints for customer-first finance everywhere. What begins as a local workaround becomes an exportable advantage.

As these companies grow, they are doing more than serving local markets. They are quietly redefining what modern financial infrastructure can look like — to build something to bridge, or even transform, the gap. In the process, these founders are showing that meaningful financial innovation often emerges not from optimizing established systems, but from building entirely new ones. What’s emerging is a new map of financial innovation — one where some of the most important ideas are being tested far from the traditional hubs of global finance.

For Endeavor Entrepreneurs, recognizing limitations is an opportunity — to help others that had the same problem as you. That’s why these companies don’t stay local for long.