Stablecoins didn’t need Wall Street

The inflection point has already happened in Elsewhere markets.

Some massive opportunities happen Elsewhere by nature.

For example, holding US dollars in an abstracted form doesn’t really seem rational if you already hold dollars day-to-day. But in markets outside major global hubs, where local currencies are volatile, banking is thin, and dollar access is restricted, having stablecoins — cryptocurrencies pegged to the value of the US dollar — just makes sense.

Users in these markets aren’t adopting stablecoins out of enthusiasm for the blockchain. They’re doing it to protect savings from devaluation, move money across borders without losing on average 6-7% to conversion and transfer fees, and pay suppliers without waiting 3-5 business days for correspondent banking to finish processing.

But stablecoins aren’t new. USDT launched in 2014. USDC in 2018. The concept of a crypto asset connected to the US dollar has been around long enough, but as of June 2026, the global fiat-backed stablecoin supply exceeds $275B, up 40x from 2020.

For the first time, stablecoins seem to be going mainstream. Here’s why and how Elsewhere is leading the way.

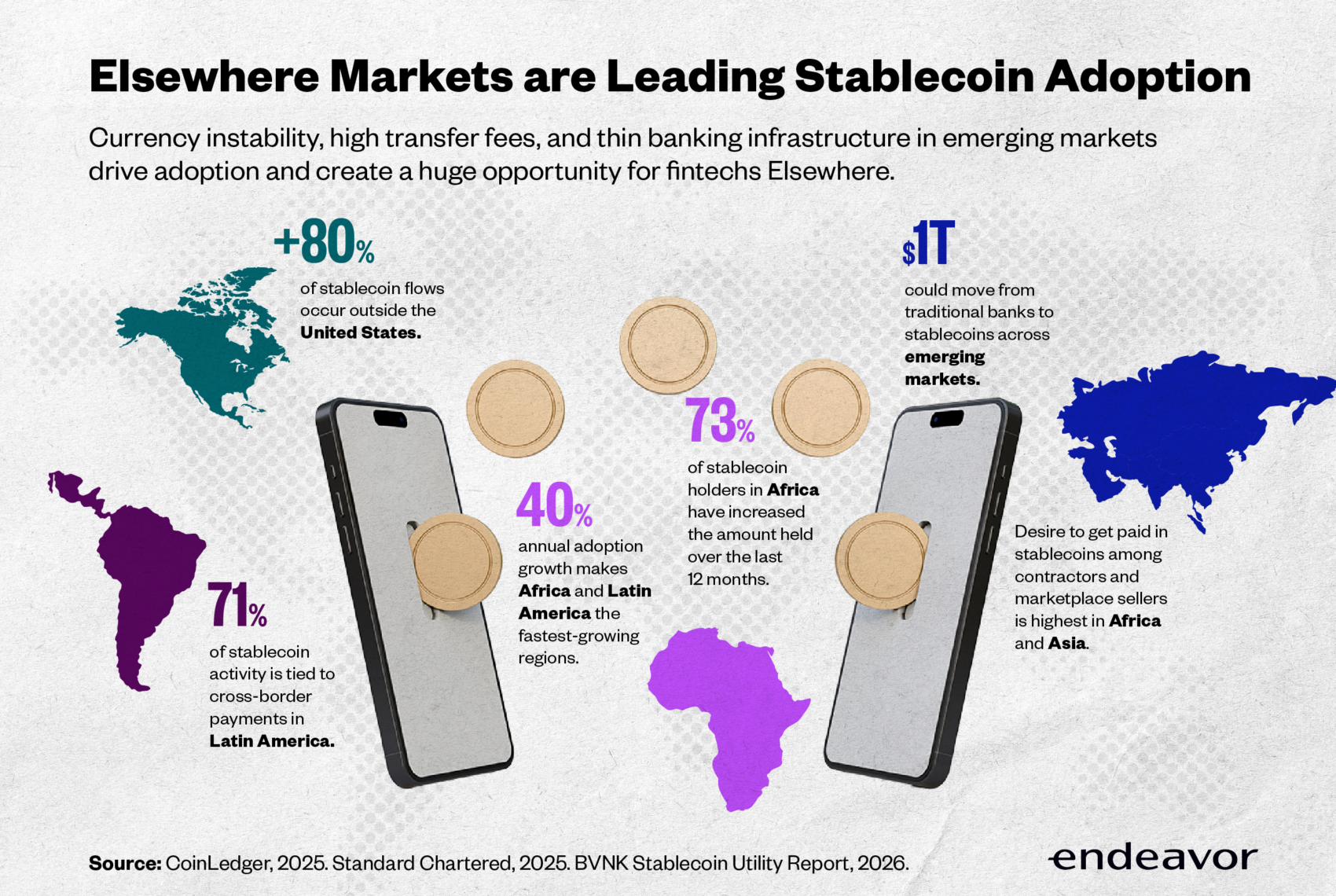

1. Where are stablecoins taking hold?

Let’s show you via simple math.

The Brazilian real lost 18% against the dollar in 2024, meaning anyone holding savings in reais watched nearly a fifth of their purchasing power for imported goods evaporate in 12 months. In Argentina, inflation has been so persistent that a basket of goods costing 100 pesos in 2020 requires roughly 3,600 pesos to purchase today. In Argentina, 60% of all crypto transactions are now stablecoin-based. In Brazil, that’s 90%.

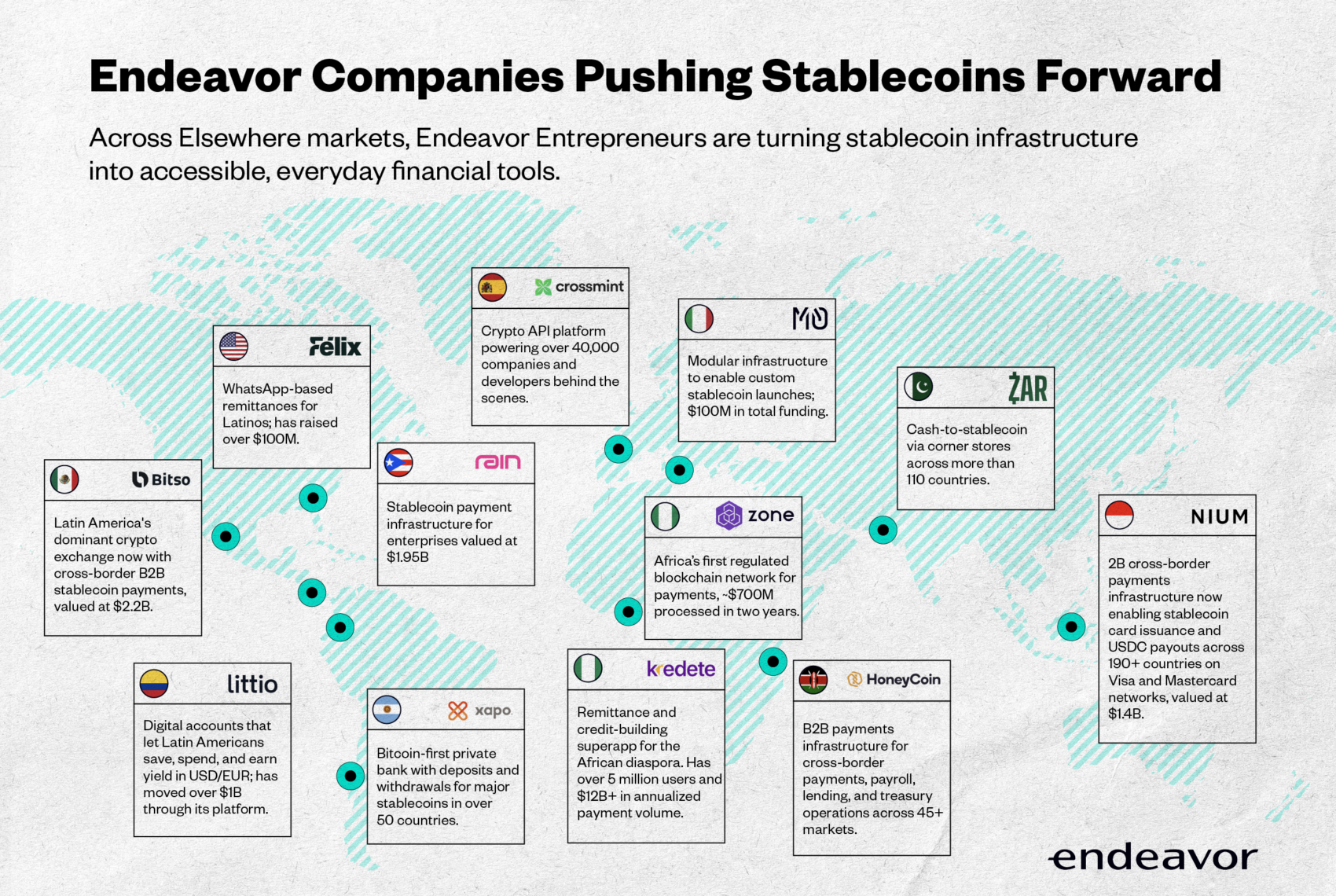

Locals in many regions end up paying a premium, whether the money is sitting still or on the move. As an example, Latino immigrants in the US sending money home were losing up to 13% per transfer in fees. Félix, an Endeavor company based in Miami, used stablecoins to cut fees to a minimum and rebuild the remittance experience to be cheaper and faster. Through a user-friendly WhatsApp chatbot running on USDC rails, it now moves $3B annually. Its results and a $75M Series B led by QED Investors in 2025 suggest the old system was long overdue for an overhaul.

The same underlying logic shows up across Africa, the Middle East, Southeast Asia, and Europe, each with different friction points. In some places, it’s not just access to USD bank accounts that is limited, but to bank accounts in any currency. Pakistani fintech ZAR sidesteps that entirely by working through the 28 million money transfer agents already embedded in these communities — the corner stores and phone kiosks people already trust — turning them into physical stablecoin exchange points.

The markets with the least access to stable financial infrastructure are the ones building the most fluency with the technology designed to replace it.

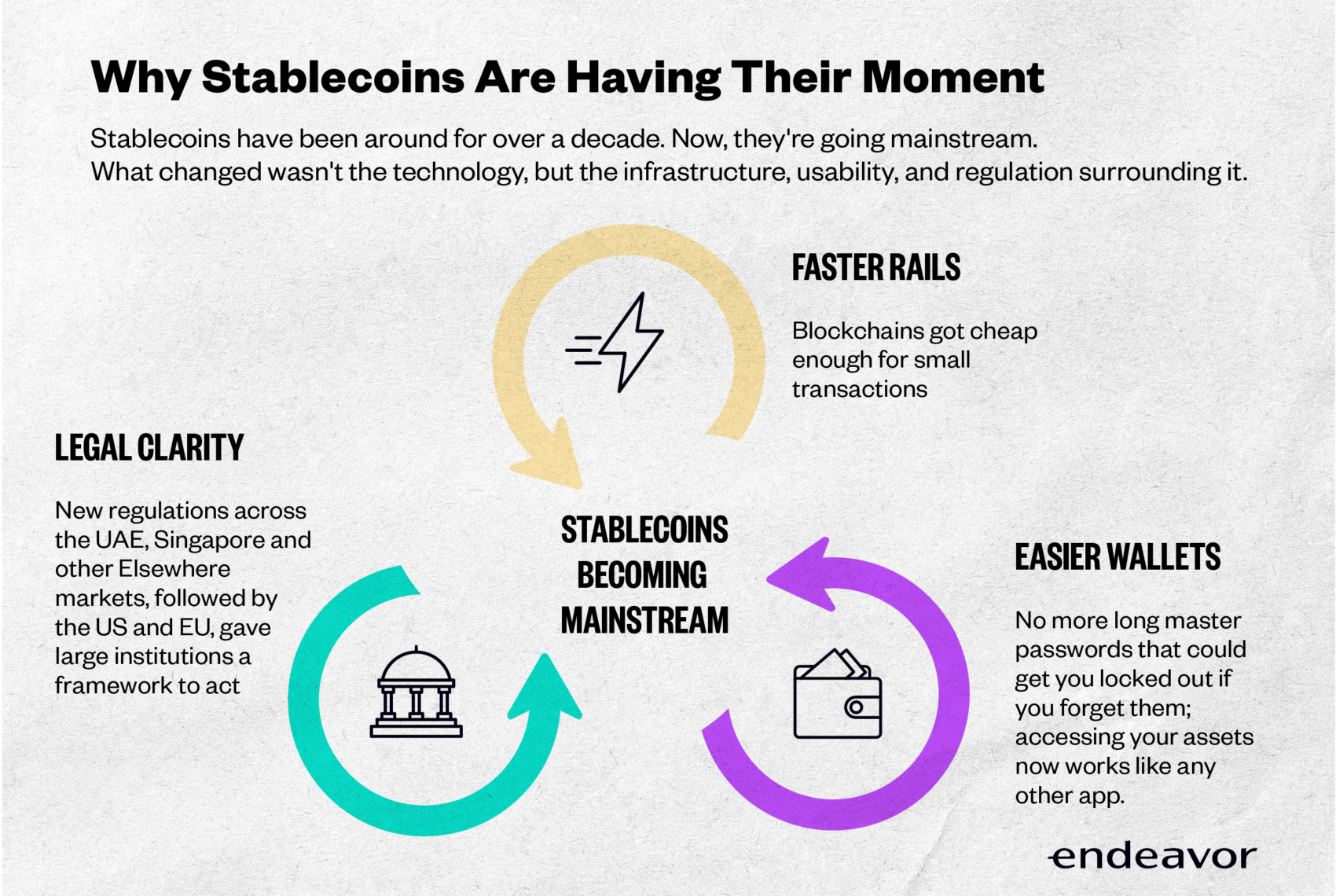

2. Why now?

Three things converged.

First, the blockchains got cheaper and faster. Early networks’ fees made small transactions cost-prohibitive. Now, Solana, Stellar, and various Layer 2 networks make it economically viable to move $50 across borders in seconds.

Second, wallets got easier. Seed phrases — the 12-to-24-word recovery strings that defined early crypto UX — were a genuine barrier and started becoming less of a thing from 2023 on, replaced by familiar login flows.

Third, regulation arrived. Elsewhere markets were among the earliest movers, later reinforced by developments in the world’s traditional financial and technology hubs:

🇦🇪 The UAE was among the first jurisdictions globally to establish a comprehensive framework for virtual assets, with Abu Dhabi launching formal regulation for crypto activities in 2018. In 2022, Dubai established VARA, the world’s first independent regulator dedicated to virtual assets.

🇸🇬 Singapore continued the trend, building one of Asia’s most mature regulatory environments for digital assets and stablecoins in 2023.

🇪🇺🇺🇸 More recently, the EU’s MiCA framework (2024) and the US GENIUS Act (2025) brought regulatory clarity at a larger scale.

🇳🇬 Nigeria also moved decisively in 2025, formally bringing virtual and digital assets within its securities framework through the Investments and Securities Act.

Before these, institutional capital stayed out. Legal status was murky. Were stablecoins securities? Could a regulator shut down an issuer overnight? Formal oversight and clarity were a trigger for companies like Visa, JPMorgan, Citi, Shopify, Stripe, and Robinhood to move seriously into the space.

" The regulatory story tells us the same as the adoption story: the markets with the most at stake moved first. Long before stablecoins became a policy priority for global hubs, Elsewhere was building frameworks, issuing licenses, and creating rules that enabled real-world use."

Kriti Sapra

Lead Manager, Entrepreneur Experience at Endeavor

Does it mean it’s perfect? No. Frameworks don’t fully align yet, and most of the world is still in a grey zone. But imperfect clarity is a significant improvement over none at all.

3. What now?

Every projection around stablecoins suggests it is still early, but accelerating quickly. Citi’s base case has the stablecoin market hitting $1.9T by 2030 — nearly 10x where it is today — with an optimistic scenario pushing that to $4T. Y Combinator now offers its standard $500,000 seed investment in USDC. Stripe, Shopify, and PayPal have all integrated stablecoin rails.

The technology is no longer waiting for adoption; adoption is waiting for the right products. But the funny thing is: Consumers rarely know they’re using stablecoins. And they don’t need to. What they know is that it’s faster and cheaper.

Rain’s Co-Founder and CEO Farooq Malik compares this with other fundamental tech and cultural changes: Before on-demand content was common, people would say “I’m streaming a movie.” Now we just call it “watching.” When we want to reach someone on the go, we don’t say “I will call you on my cellular phone”. Whether it’s through a carrier, on Facetime, WhatsApp, or even on Zoom, it is simply… a call.

" We think that this is the next step. We're gonna call it money, hold it like money, send it, invest it, spend it like money."

Farooq Malik

Co-Founder and CEO of Rain

The demand is there. Rain alone saw a 20x growth in revenue and volume in 2025 and is valued at almost $2B. For global expansion and integration to feel complete, however, three things still need to come together: merchant acceptance at scale, a user experience indistinguishable from any other payment app, and regulatory harmonization.

Entrepreneurs Elsewhere are best positioned to drive all three. They already know how to convert merchants or how to build positive experiences, no matter the obstacle, and regulators in Singapore, the UAE, and Japan moved faster than Washington did. Hard problems, solved in hard places, have a way of becoming the blueprint. Soon, stablecoins won’t need a separate name anymore. It’ll just be money.

Featured Stories

Japanese entrepreneurs are leveling up: Endeavor CEO Linda Rottenberg explains how

The Collapse That Forced Proptech’s Boldest Founders to Reinvent Everything

Elsewhere, fintech is solving problems Silicon Valley never had

Related Articles

Japanese entrepreneurs are leveling up: Endeavor CEO Linda Rottenberg explains how

The Collapse That Forced Proptech’s Boldest Founders to Reinvent Everything