There’s Nothing Wrong With Raising a Down Round

When valuations get too inflated, down rounds pull the market back to earth. We don't have to love them, but we shouldn't fear them.

Imagine you’re the founder of a successful tech startup. You’ve achieved product-market fit and raised a financing round in 2021 at a record valuation. There were even articles written about your company in TechCrunch! Since then, revenue has doubled and you’re now looking to raise another round. Unfortunately, the venture capital landscape has changed, and despite its growth, your company is worth less today than it was two years ago. What do you do? Do you accept reality and raise capital at a lower valuation, knowing it may harm the perception of your business, or do you avoid it at all costs?

Raising a down round is taboo in the venture capital world, forcing founders and early investors to confront a number of tough questions and feelings. It shouldn’t be so scary. Much like in the public markets, there are a number of reasons why private companies may go up and down in value. When valuations get too inflated, down rounds pull the market back to earth. We don’t have to love them, but we shouldn’t fear them.

" When valuations get too inflated, down rounds can pull the market back to earth."

The End of Easy Money

Thanks to record low interest rates and an abundance of cash over the past decade, venture capital exploded, sprinkling the globe with innovative startups all eager to scale. Traditional investors were joined by hedge funds, crossover funds, and other new VC entrants hungry for yield—flooding the market with investment dollars.

With ample cash chasing limited deals, investors began making riskier bets and allowing entrepreneurs to dictate the price and terms of their funding rounds. An entire generation came to believe that private market valuations only moved in one direction (up!). Interest rate hikes around the globe have now set that combustible market ablaze.

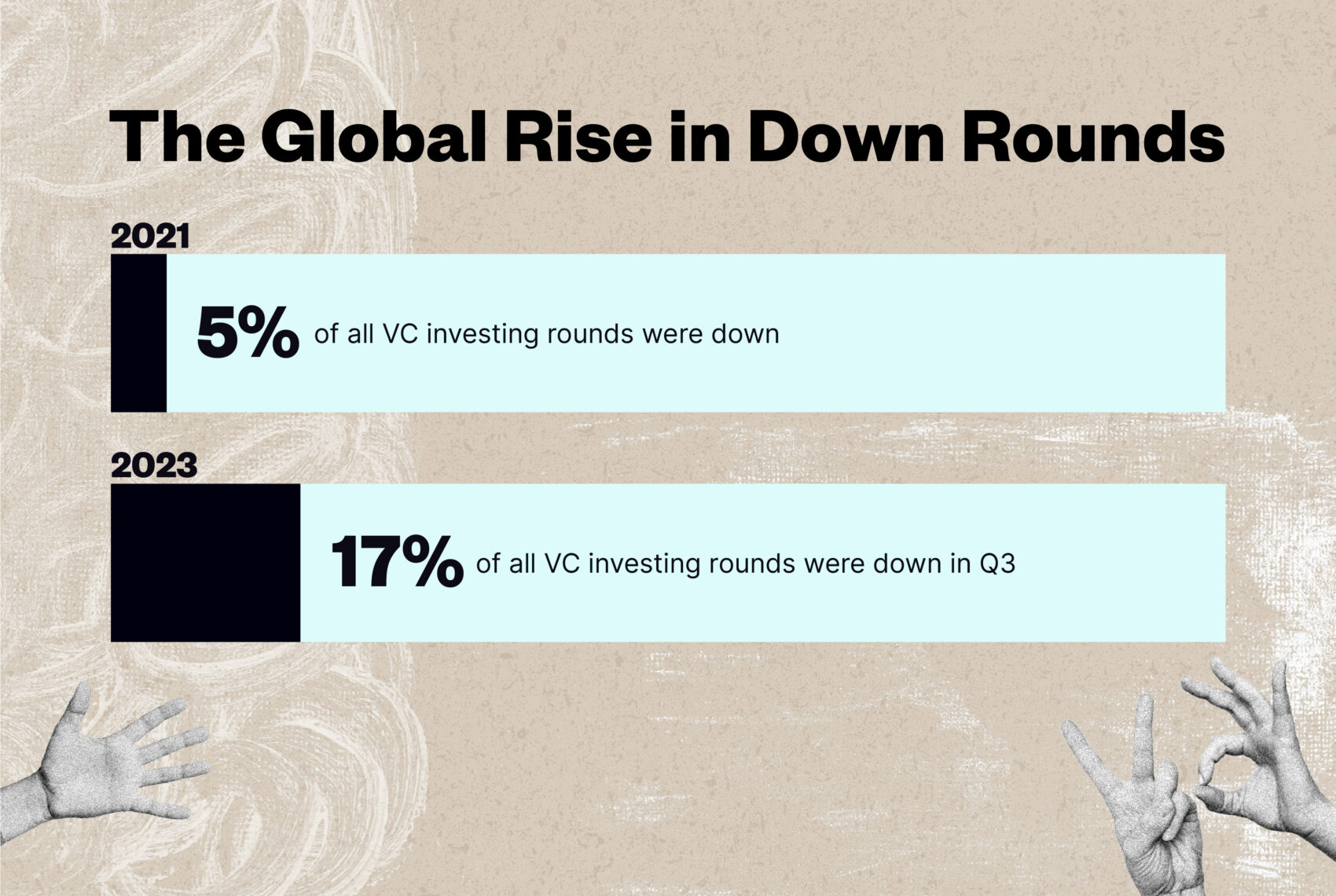

Down rounds—or a private company selling additional shares at a lower price than its previous financing round—are a new reality we must accept. In Q1, Q2, and Q3, they accounted for nearly 17% (nearly 1 in 5) of all global venture investing rounds, compared to just 5% in 2021. And they’re trending upward.

Though they’re more common today, down rounds still carry a stigma. No founder aspires to a down round, and many are doing everything possible to avoid one. Some founders are decreasing burn to extend their runway, hoping the market will recover before they need more capital. Others are turning to alternative funding sources like insider-led rounds, extension rounds, bridge financings, and/or venture debt.

Creative founders are even buttressing their deals with added structure and complexity (e.g. 3x liquidation preferences) to create the illusion of a flat or up round, while limiting downside for new investors. These types of rounds are often a greater sign of distress than holding an honest down round, and they muddy a company’s cap table—placing founders and early investors in an unfavorable position.

The Choices We Make

It doesn’t need to be this way. In public markets, the value of companies moves up and down by the second. Public companies have “down rounds” that last days, months, or years, and we understand that it’s not always their fault because we see the entire market moving up and down with them. Unlike in the public markets, private market valuations are less fluid, so even a mostly harmless down round can affect a company’s perceived value for years, but only if we let it, argues Shu Nyatta, founder and managing partner at Bicycle Capital and former managing partner at Softbank. He joined us at a recent Endeavor Catalyst event.

“There’s this interesting idea that [public and private] markets are totally different,” says Shu. “But it doesn’t make any sense to me that the private market can’t move up and down in the same way that the public markets do.”

While not aspirational, Shu argues that a down round should not signify that something is wrong with a company. At face value, it could simply mean the company is raising capital at a time when multiples and valuations are naturally contracting, and investors are more risk-averse—much like how up rounds indicate the opposite.

Shu also notes how odd it is that private company valuations are glorified so much. “You don’t see Apple saying we’re a trillion dollar company. Come join us. It’s not a thing,” he says. “The price is the price, and the company talks about different things. But for venture [capital], for some reason, advertising valuation is a way to get credibility and attract employees, which, by the way, is backwards. When you announce a high valuation, [investors have already] missed it. They should come when you announce a low valuation, you should say we’re the lowest valuation we’re ever going to be. Come join us!”

Glimmers of Change

In mid-2022, Axios Pro Rata made an interesting point: If everyone raises a down round, does anyone really notice? Do they still have the same reputational damage if they’re happening across the board? In current conditions, down rounds are a reality many companies will face in the near future—all over the world.

“I think if you [take a down round], it’ll be a relief because you won’t have this crazy thing you’re supposed to be that you’re pretending to be,” says Shu. “You move on with your life instead of the charade of trying to somehow justify this number that you didn’t set.” For those who raised money during peak years like 2021, their “number” (valuation) was a product of record low interest rates and abundant capital.

Facebook (now Meta) famously raised a down round in 2009, lowering its valuation by a third from $15 billion to $10 billion. It’s worth $800 billion today.

More recently, the “buy now, pay later” company Klarna, raised a round at an 85% valuation drop in 2022. Sequoia partner Michael Moritz explained that Klarna’s lower valuation is “entirely due to investors suddenly voting in the opposite manner” to the way they voted previously. “The irony is that Klarna’s business, its position in various markets and its popularity with consumers and merchants, are all stronger than at any time since Sequoia first invested in 2010,” Moritz said in a press release.

" Facebook famously raised a down round in 2009, lowering its valuation from $15 billion to $10 billion."

There are glimmers of a change in mentality. Some private companies have begun proactively lowering their valuations, instead of waiting to be re-priced in a funding round.

In the Endeavor Catalyst portfolio, European fintech darling Checkout.com decreased its internal valuation from $40 billion in early 2022 to $11 billion in late 2022, and most recently to $9 billion in mid 2023. These cuts came in spite of a growing business. “While this may appear negative, it actually offers the opportunity to capture more financial upside over time for newly issued shares at a lower strike price, hence a good thing,” writes Kerry Van Voris, Checkout.com’s chief people officer.

“It could all even out in the end” when it comes to lowered valuations, says Clete Brewer, managing partner at NewRoad Capital Partners. “Founders who may have gotten away with too little dilution in an earlier round may now be compensating by taking a bit more [dilution] …. Of course, this assumes you live to fight another day.”

Other growth stage companies, like payments giants Stripe and grocery delivery company Instacart, lowered their internal valuations in 2023.

" There are glimmers of change. Some private companies are proactively lowering their valuations instead of waiting to be re-priced in a funding round."

Of course, not all investors ultimately emerge as winners, as was recently seen in Instacart’s IPO. Nonetheless, accessing the public market at an acceptable price is an important milestone that brings opportunities for continued growth.

The Drive to Survive

In startup land, the name of the game will always be survival, and many founders, especially those in emerging or underserved markets, may not feel like they even have the privilege of taking a down round as they try to make payroll. And while it may feel darker, harder, and more uncertain than they did just 18 months ago, we can take solace knowing that the most exciting and generation-defining startups are often built in the toughest of times.

Watching a down round destroy a company’s perceived value is painful, whether you’re a founder or investor, but it’s important to remember that a financing round is not an outcome, it’s just another mile marker along the way.

Updated January 2024 with the percentage of down rounds in Q3 of 2023.

Featured Stories

Silicon Valley got crowded again. Here are 400 reasons why we’re staying Elsewhere.

2025 Endeavor Catalyst Annual Report: A Look into Global Venture Capital

The Race for the Next AI Success Story Is Not Where You Think

‘I don’t want to talk to any of you’: Addressing the VC Blindspot

Related Articles

Silicon Valley got crowded again. Here are 400 reasons why we’re staying Elsewhere.

2025 Endeavor Catalyst Annual Report: A Look into Global Venture Capital