Pulled Term Sheets, Pinched Valuations, But No Lack of Entrepreneurial Conviction: Tracking Latin America’s VC Downturn

How will Latin America startup hubs weather the chill in startup funding? We rounded up quotes from investors, entrepreneurs, and analysts to detail the challenges as well as the hopes and opportunities.

How will Latin America startup hubs weather the chill in startup funding and the changed power balance between entrepreneurs and investors? We rounded up quotes from investors, entrepreneurs, and analysts to detail the challenges as well as the hopes and opportunities.

Jimena Pardo has been on both sides of the table. As an entrepreneur-turned-VC, she’s keenly attuned to what founders have to go through when times are tough. And some of what she’s seeing today across Latin America’s startup ecosystem isn’t exactly pretty.

Overall, round sizes, and valuations are all off sharply, says Pardo, who joined ALLVP, a Latin America-focused firm, earlier this year.

And, some VCs have started to turn the pressure up on the region’s founders.

Pardo has seen arm-twisting behavior grow: some VCs are seizing the opportunity to negotiate more aggressively for investor-friendly terms, especially when it comes to valuations.

Worse, in a few instances, she says, entrepreneurs have approached her to commiserate after investors backed out of deals, reneging on verbal commitments or pulling term sheets.

“This is outrageous,” says Pardo, who in the 2010s co-founded Mexican car-sharing startup Carrot.

" It deeply hurts the entrepreneur, and the ecosystem we’re building. This kind of behavior should be aired when it happens, and it should have reputational repercussions. "

Jimena Pardo, Partner at ALLVP

Welcome to what might be called the global VC vibe shift. The correction is global, but Latin America has seen an especially sharp change.

After a volcanic 2021 that spewed a record amount of dollars on the region, the funding market cooled off quickly starting in March and April of this year (as we’ll see, however, deal volumes have remained remarkably resilient).

Lucas Abreu, a VC investor in Brazil who writes a newsletter on Latin American VC trends, marveled at how suddenly things seemed to turn in his May 25th, 2022 newsletter.

" Winter came suddenly, he wrote."

Abreu also noted that many of the factors underlying the global downturn are present domestically in Brazil itself (as they are in other Latin American economies).

That is: higher interest rates, rising inflation, and lower multiples for comparable, publicly-traded tech companies.

Of course, perspective is needed: the roof is not falling.

That message is delivered emphatically in an interview with Endeavor Global by Laura Gonzalez-Estefani, CEO at Miami-based VentureCity, a global accelerator which has worked with early-stage companies across Latin America (and elsewhere).

She believes 2021 was an anomaly, the market distorted by “tourists” and fickle global investors pouring money into Latin American startups. What we’re seeing now is more of a return to normal.

" Last year was absolutely not a representative year. Speaking to founders, I’d say, ignore the noise, keep your head down, and keep the focus on building great products for your customers. There’s never been a better time to be a startup founder in Latin America. "

Laura Gonzalez-Estefani, CEO at Miami-based VentureCity

Of course, as Gonzalez-Estefani acknowledges, the sudden correction is going to be tough going for many.

Founders will find themselves trying to grow into 2020 and 2021’s high valuations. If they do need to raise, the funding environment will not be nearly as generous.

“Startups that raised cash at peak valuation, for example last July last year, will have to accept a reduction [in valuation] if they need more money this year,” said Sergio Furio, founder of Brazil’s fintech unicorn, Creditas, speaking to Reuters.

We dug through hundreds of reports, blog posts, tweets, articles, and investor updates to distill the principal trends in each region into a single digestible article. Our hope is that entrepreneurs will turn to this material for information on what’s happening in the region, as well as forward-looking insight into how to navigate the cross-currents.

The retreat of investors from Asia and North America

Already in March 2022, investors were backing out of deal commitments as they felt power shift back in their favor, according to Rajeev Misra, CEO of Softbank Investment Advisers.

The SoftBank Vision Fund, which Misra manages, has invested large checks in hundreds of startups across the Americas, Asia, Europe, the Middle East, and Africa.

“In the last few weeks in the private markets, we have seen certain investors back out after verbal commitments,” Rajeev Misra said in March 2022 to India’s Economic Times.

" Also, the power of capital has shifted back to the capital provider. Before, I had to go and beg … Founders had multiple choices of investors sending them term sheets in one week, without detailed due diligence and so on, where they decided the price and the valuation. That has changed."

Rajeev Misra, CEO of Softbank Investment Advisers

SoftBank, Misra added, had slowed its pace of dealmaking and was scrutinizing companies’ metrics more closely.

New York-based Tiger Global Management also telegraphed its intent to back away from late-stage startup investing as early as 2022.

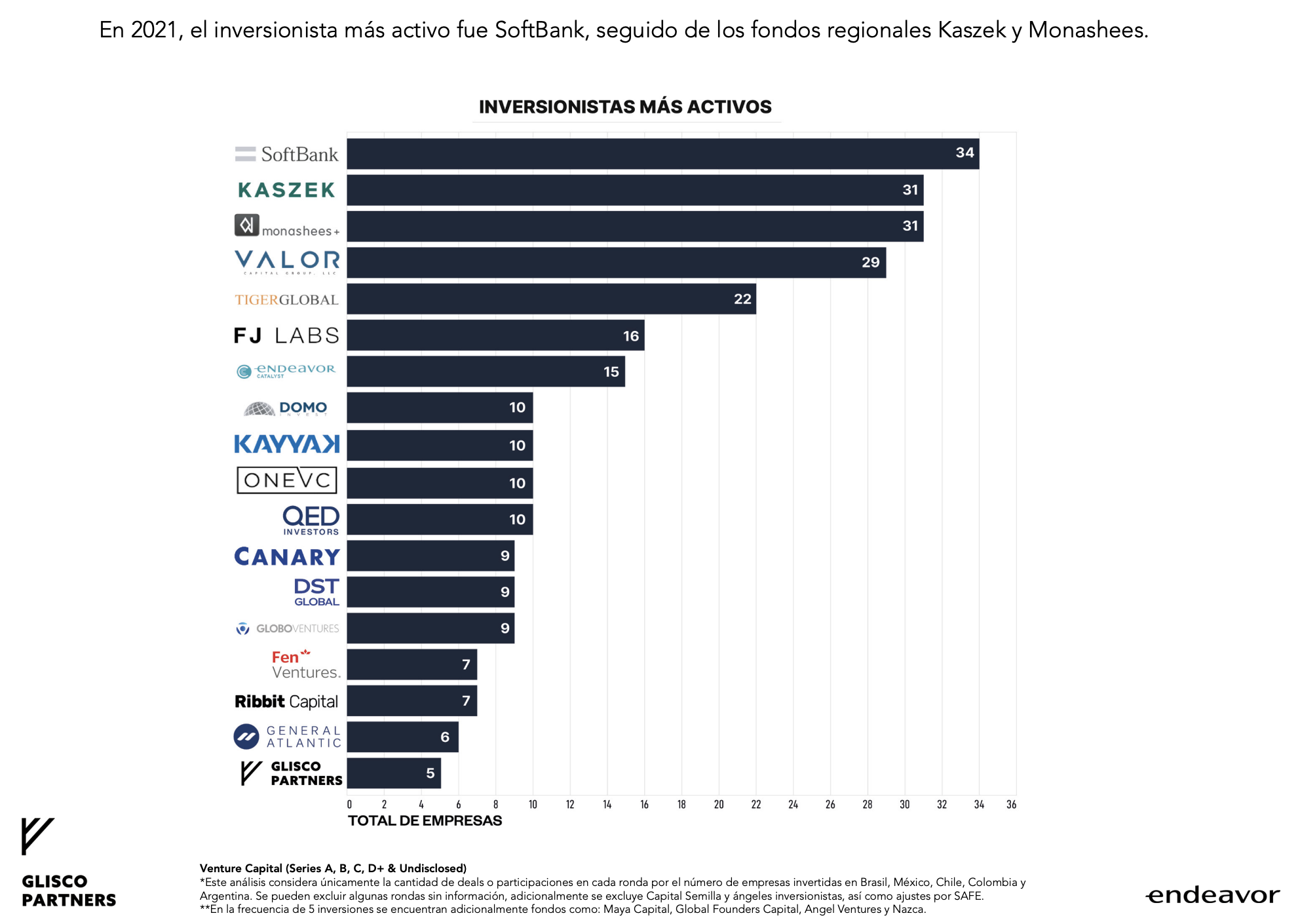

As shown below, these two firms together accounted for some 63 checks into Latin American startups in 2021, according to data collected by Endeavor Mexico and Glisco Partners. Their deep pockets helped nearly quadruple the VC dollars going into the region in 2021 ($20.2B per CB Insights, versus 2020’s amount).

Neither investor made CB Insights’s list of most active investors into Latin American and the Caribbean for the second quarter of 2022.

Eduardo Vasconcellos, who is a vice president at Singapore’s sovereign wealth fund, GIC, called this risk-off environment Latin America’s “New Normal,” in a May 5, 2022 of his newsletter.

“I don’t know any investors who want to do new investments today on the same terms they did in 2021,” wrote Vasconcellos. In fact, he added, he has seen deals renegotiated as the macroeconomic environment deteriorated: “There’s plenty of companies that had to renegotiate deals because the lead investor lost interest in the round.”

Pardo, of ALLVP, says she expects SoftBank and Tiger to wade back in gradually. Even if this year it is mostly with follow-on investments.

“The opportunity in Latam is still very juicy,” says Pardo, who spoke to Endeavor Global in an e-mail interview, given the talent and tech-adoption tailwinds.

A deal in May proves her point nicely.

In that month, Bogotá-based real estate-tech startup Habi announced a $100M Series C round. SoftBank VisionFund Latin America led the round, alongside VC firm Homebrew (SoftBank also had led the Series B). Tiger Global also participated in the new round. It ended up being the largest round into the region in the second quarter.

Brynne McNulty, Habi’s co-founder, detailed in the funding announcement how the company had gone on the offensive in 2022 rather than playing defense: it had made several acquisitions early in the year, expanded to new cities, and appointed a new CFO.

Habi’s raise shows that the region’s quality founders can still attract investment, regardless of the capital climate, according to Juan Franck, SoftBank Latin America Fund’s managing partner.

" There is significant investor appetite available for proven business models with strong unit economics and a clear path to profitability. Even during the most difficult fundraising environment of the last 10 years. "

Juan Franck, SoftBank Latin America Fund’s managing partner

In August 2022, meanwhile, Tiger Global was active at the seed stage: the group co-led a $7M seed round into Mexican retail wholesaling marketplace Miferia and led a $3M round into an Argentina-based subscription and payment collection startup, Rebill.

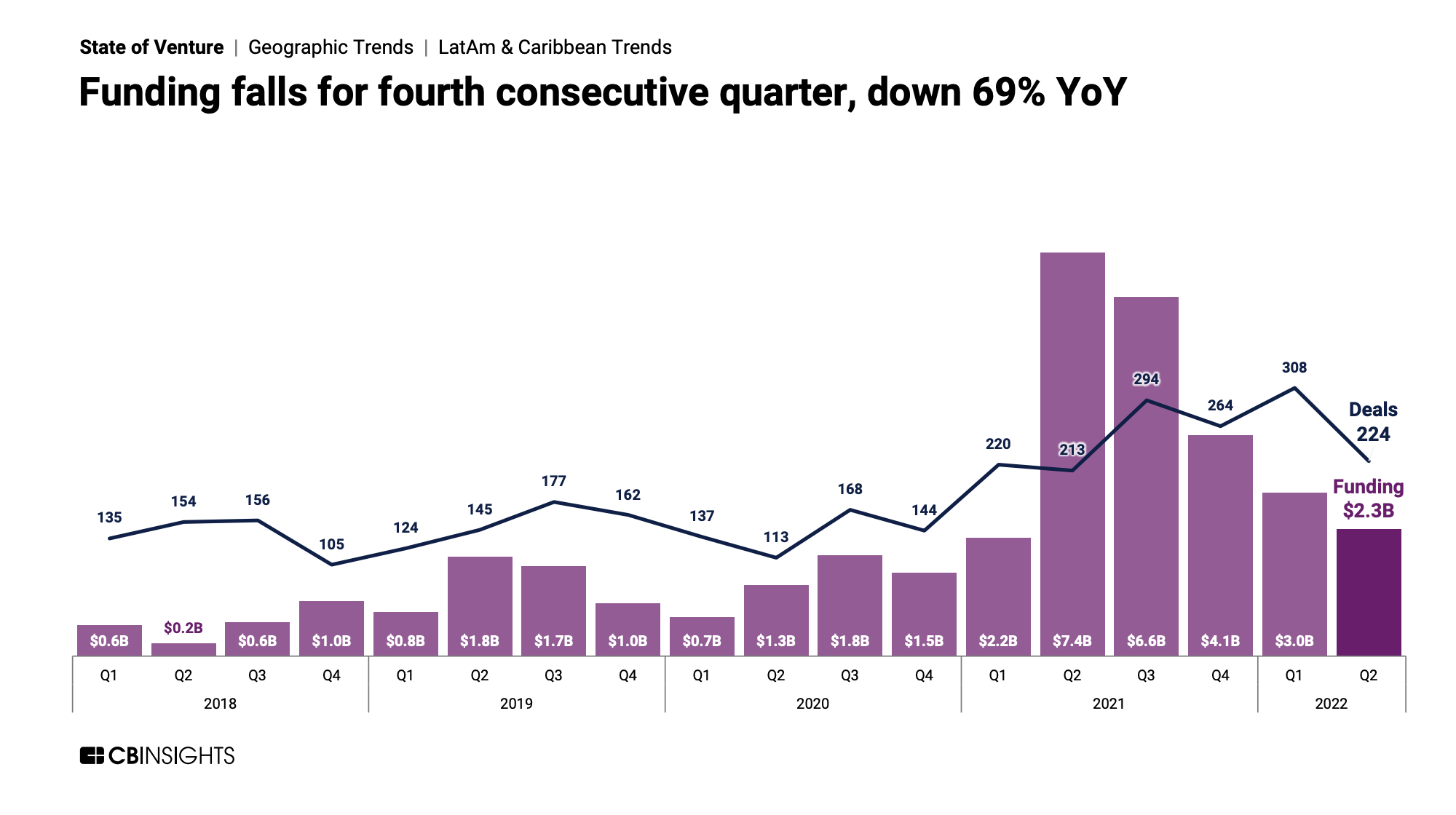

The question in Latin America as the downturn began was whether funding trends would hold some of their gains and manage to avoid a return to 2020 levels or below.

How bad is it actually? What the data shows

By all accounts we are already at least five months into this downturn, and in fact it looks like LatAm will handily beat 2020 for deal activity and dollars even if funding dollars will be down compared to 2021.

Already, halfway through the year, there have been nearly as many dollars and deals as there were in all of 2020.

What does the new normal look like?

An earlier report from Endeavor Mexico and Glisco Partners, which tracks funding into a representative cohort of Latin American startups and markets, also found that deal activity and funding levels for the first third of 2022 actually remained well above 2020 levels.

Still, Enrico del Río, head of intelligence at Endeavor Mexico, predicted in an interview with Bloomberg Línea that the region would see significantly less financings of $50M and above in 2022 than in the previous year. He said that would certainly depress funding levels overall for the year, since these larger rounds accounted for 79% of the capital invested in 2021.

While VC markets are absolutely not frozen, and early stage deals in particular are still getting done, what’s clear is that the rules of the game have changed.

More leverage for investors

In just a few months, we’ve seen an erosion of the “founder-friendly” paradigm that was in effect globally. In the flush times created by rock-bottom interest rates, VC firms sought to outdo one another in how accommodating they’d be to founders’ desire for control, high valuations, and runway.

Structurally, higher interest rates make VC investments less forgiving. Capital allocators can move into assets like bonds that now are more competitive from a yield perspective. Also, in a high-rate environment future profits are priced at lower levels in the present, creating gravity for valuations.

These and other factors have instilled caution in investors, and will also nudge them toward early-stage investing when they do wade in, according to analysts. That’s partly because early-stage rounds can be done with smaller checks and at relatively tiny valuations and also because by definition they are longer term bets, meaning interest rates are less of a factor.

But, even at the early stage, investors will have an eye toward managing risk more directly, i.e. working with boardrooms to take the steering wheel away from founders to some extent.

“(Investors will) need to have greater control of the operation,” Roberto Kanter, a business professor and economist at FGV in Brazil, told Bloomberg Línea. “They will want to have a hand in the business’s evolution from the beginning.”

While perhaps it’s healthy for there to be more business discipline in the system overall, that’s not necessarily going to be welcome news to individual entrepreneurs, Kanter added.

While many “wartime” decisions will happen behind closed doors, it’s not a leap to predict this downturn will lead to tough conversations and executive reshuffling. With more institutional investors pushing into the early stages and wary about their portfolios’ overall quality, it’s likely entrepreneurs will see more interference.

There will be meddling, and perhaps even boards that go against founders in major decisions or even seek to force them out in favor of seasoned managers.

On top of smaller checks, and pinched valuations, entrepreneurs should expect term sheets to take considerably longer to come together.

" "Begin your conversations on the next round ahead of the normal schedule", wrote Vasconcellos, of GIC, in his newsletter. "Funds are taking longer to sign checks, and you have to get ahead of that." "

Downturn tactics menu: Pivots, layoffs, retrenchment

To conserve cash and survive the “winter,” Latin American companies have a range of options, starting with the most obvious such as negotiating better deals with vendors and closing sluggish product lines and verticals.

Layoffs are only the most obvious lever to pull. Layoffs.fyi has tracked layoffs at 50 startups in Latin America since Covid-19 broke out, and has tallied a total of more than 6,800 lost jobs in the region.

Brazil drove the most of these, with Colombia, Peru, and Argentina also represented among markets shedding employees.

Of course, companies with different levels of financial health and customer traction will face different sets of trade offs and choices.

In June 2022, as the global VC downturn accelerated, Mexico City-based VC firm ALLVP released a framework meant to help entrepreneurs calibrate to the new reality depending on their runway and metrics.

" "From where we stand, we believe that the most important thing for startups to do at this moment is to ensure survival,” write the authors, Nicolás Hereen And María Fernanda González. “There are better times ahead, but to enjoy them, founders must be disciplined in order to make it through to the other side.”"

The framework allows startup leaders to bucket themselves, depending on their cash position and growth metrics, to determine their overall strategic posture.

- Startups with less than 24 months in cash runway that are not growing should reevaluate all options. “They will have a hard time raising additional capital now that investors have become risk-averse,” the authors say. They may have no choice but to cut costs as much as possible, even while taking a last-ditch shot at achieving growth.

- Startups with more than 24 months in cash runway that are not seeing significant growth should pivot in pursuit of product-market fit while avoiding the temptation to spend on headcount or marketing.

- Startups that have less than 24 months in runway and are growing quickly should consider a raise to extend runway even if it means offering attractive terms to investors. Venture debt is also an option to explore to minimize dilution.

- The fortunate companies with more than two years of runway and positive growth should focus on their core business, while keeping a close eye on efficiency, in order to take advantage of the opportunity.

Some founders may decide to close down, return money to investors, and start afresh. But, if survival during the downturn is a strategic imperative, that’s partly because the authors are bullish on structural tailwinds.

" In the long-run, technology will still be the most important driver for progress throughout Latin America."

Nicolás Hereen & María Fernanda González

The duration of the downturn is anyone’s guess — analysts’ estimates we collected range between 12 to 36 months total — but the strong belief among nearly all market participants is that the companies that tough it out will be in an enviable position.

Long-term tailwinds

Despite the chill in VC funding at a high level, there’s a host of reasons why investors, governments, and founders are still bullish on the region.

In Latin America, consumers and businesses are relatively early on the adoption curve when it comes to technology and internet-based services.

Not only that, but incumbents often control large market share in key industries, and are vulnerable to disruption from software- and app-centric products.

Specifically, software-powered services like digital payments, online education, and e-commerce still have low penetration rates in Latin America, says Franck, of SoftBank.

" “Startups aren’t just growing (when) the economy is growing,” adds Alfredo Castellanos, managing partner of Mexico City-based Glisco Partners, “but fundamentally they are growing because they are gaining market share from traditional companies, and that phenomenon isn’t going to stop.” "

In fact, Castellanos, whose firm co-authored the report on Latin America VC funding trends with Endeavor Mexico cited above, implied that the economic slowdown may even accelerate startup-led disruption.

To be sure, incumbents often compromise on quality, innovation, and marketing during downturns. That leaves room for nimble startups — those still alive, of course — to win over customers with higher-margin, tech-enabled products and services.

Talent — particularly technology, design and product hires — which became so scarce in the go-go years will likely become more plentiful and inexpensive.

Meanwhile, the advantage of the massive year in 2021 is that Latin America has seeded a region-wide network of investors, companies, entrepreneurs, and talent that will continue to fuel the ecosystem in years to come, irrespective of valuations or investors’ whims.

The Endeavor Mexico and Glisco Partners Panorama report counted 31 Latin American unicorns, and an additional 130 companies that had reached a valuation of $100M or higher by year-end 2021. While some of these companies may founder, many will succeed, exit, and lay the groundwork for future innovation.

Francisco Alvarez-Demalde, the Argentine co-founder of Riverwood Capital, which invests frequently in the region, put it this way in a LinkedIn post: “Digitalization and innovation will continue to transform our lives, but capital is back to having some cost.” He added:

" Like in other cycles, periods like this can become a big opportunity for building, consolidating market leadership, recruiting talent ... Keep building! "

Featured Stories

Silicon Valley got crowded again. Here are 400 reasons why we’re staying Elsewhere.

2025 Endeavor Catalyst Annual Report: A Look into Global Venture Capital

The Race for the Next AI Success Story Is Not Where You Think

‘I don’t want to talk to any of you’: Addressing the VC Blindspot

Related Articles

Silicon Valley got crowded again. Here are 400 reasons why we’re staying Elsewhere.

2025 Endeavor Catalyst Annual Report: A Look into Global Venture Capital