From Street Markets to E-commerce Giants: B2C Dominates Southeast Asia’s Economy

Anyone reading about the Southeast Asian innovation ecosystem in 2023 would have come across plenty of negative headlines. VC funding in the region was down 50% from its pandemic peak in the first half of 2023, pressuring companies to reach profitability. Layoffs increased across the region, and many previous investor darlings, like Halodoc and Lazada have pivoted or pulled back. Some, like Flash Coffee, have filed for liquidation in some underperforming markets.

Does this mean the market conditions and innovative energy that created regional success stories like Malaysian decacorn Grab and Indonesian super app Gojek are over?

While the current tech winter is definitely forcing companies to get creative and find new routes to sustainable growth, at Endeavor Catalyst we remain hugely optimistic about the market, particularly for B2C companies.

Southeast Asia has a young, techcentric, social media-loving population, and with the fast adoption of digital payments since the pandemic, brands have thrived. Ecommerce has seen a significant boost from startups in the region improving the entire sales cycle, from discovery (Indonesia’s Bukalapak and Singapore’s 99.co) to fulfillment (Kargo, Shipper, and Janio).

“I’ve witnessed firsthand the dynamic growth and vibrant potential of the B2C sector in Asia,” Linda Anggrea, founder and CEO of clothier ButtonScarves, said. “The region’s rapidly expanding middle class and increasing digital connectivity are driving unprecedented demand for consumer-focused businesses. Looking ahead, I believe Asia holds a good promise for B2C companies, particularly those that leverage technology to enhance customer experiences and sustainably expand their reach.”

" With high-quality products, B2C companies are still entering and succeeding the market, the B2C boom here is not fading anytime soon. "

Trends powering the B2C boom in Southeast Asia

Southeast Asia is home to 660 million people, making it the third-largest collective consumer base in the world, after China and India. And this youthful population of hundreds of millions is digitizing at an incredible rate as previous startups have built digital payments, marketplaces, and logistics solutions to allow more and more aspects of daily life to take place online.

The economy SEA 2022 report from Google, Temasek, and Bain shows Indonesia’s digital economy will reach $130 billion in 2025. The issuance of new digital bank licenses in Malaysia seems likely to further accelerate the shift towards mobile banking in the country already begun by early innovators like Maybank. This move builds upon the already high number of active internet users (80%) and mobile phone penetration (84.2%) in the country. We expect the number of users of digital payments in Malaysia to balloon to 20.02 million by 2027.

The Philippines has been slower to adopt digital banking. In spite of favorable demographics, 78% of eligible Filipinos are unbanked or underbanked, which may explain why fintech companies are now attracting the most funding from investors there. The potential for growth is vast and some startups are already seizing the opportunity: Coins.PH is the leading mobile wallet and cryptocurrency exchange in the Philippines with over 16 million users.

But If consumer fintech is emerging in the Philippines, e-commerce is booming. The Philippines is the fastest-growing e-commerce market globally. Sales now stand at $17 billion driven by the country’s 73 million active internet users. Consumption expenditure is 91% of GDP, well above the average of 60%.

Gaming is another bright spot in the region. In Vietnam Amanotes has three million app downloads and 100 million active monthly users, making it the number one music games publisher in the world and the number one mobile apps publisher in Southeast Asia. Sky Mavis, another Vietnamese company, built Axie Infinity into the number one blockchain game of its kind with over 2.5 million daily users in 2022.

With more and more potential customers across Asia looking to do more online and more and more of the necessary infrastructure required for these transactions being built, the stage is set for consumer-facing companies to continue to boom in Southeast Asia.

" The region boasts a young, tech-savvy population comfortable with online transactions and brand discovery. This is a fertile ground for disruptive digital-first consumer brands. "

Eric Woo

Growth stage Investor at Venturi Partners

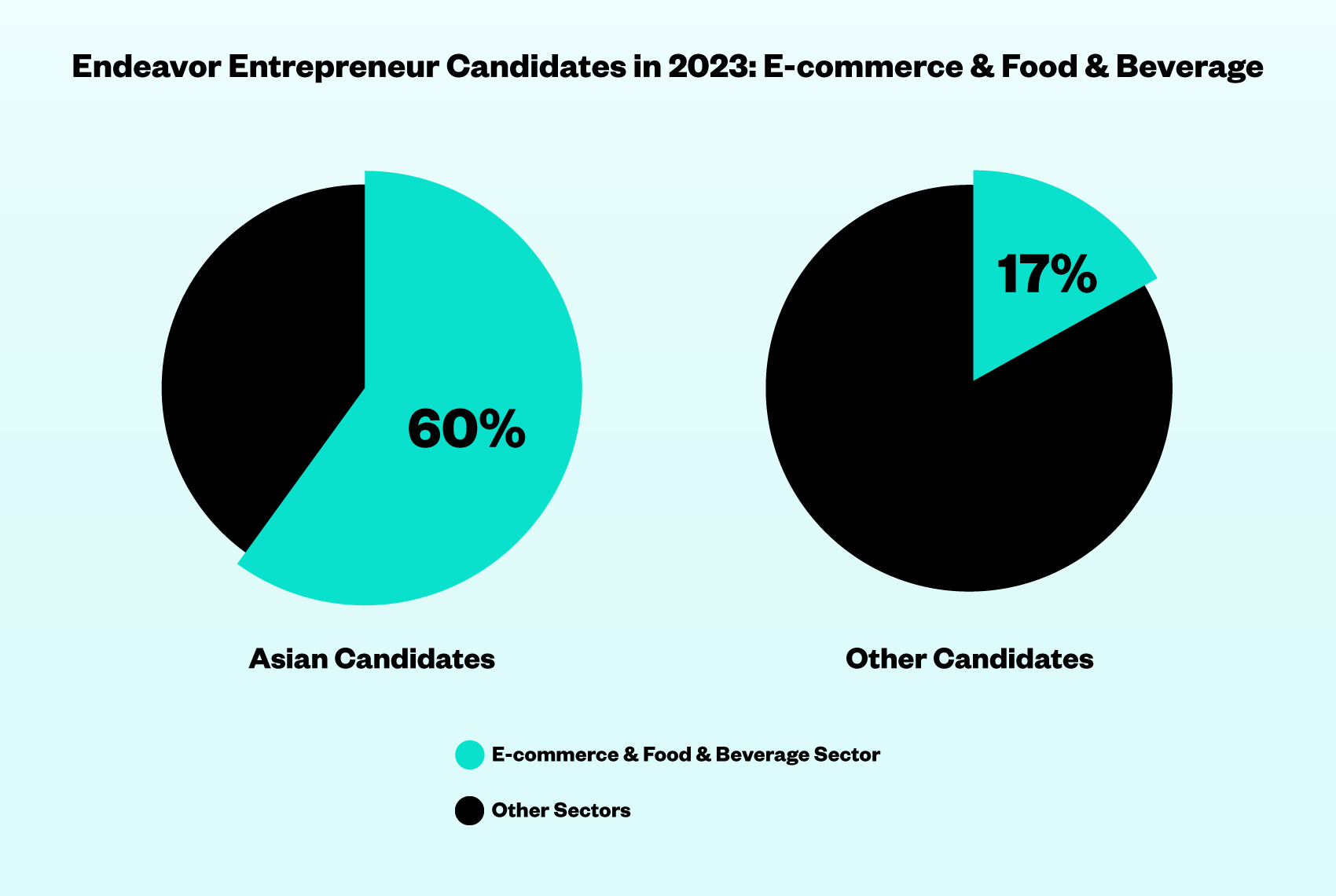

At Endeavor we’ve seen this reflected in the applicant pool for Endeavor Entrepreneurs: 77% of the companies selected from Asia in 2023 were consumer-facing. Almost 60% of all Asian candidates at our International Selection Panels last year were in the e-commerce or food & beverage sectors, compared to 17% of companies in these sectors from the rest of the world.

Challenges and changes ahead

The market fundamentals suggest there is a lot of room for B2C innovation and growth in these markets. But while the medium-term outlook is excellent, it is important to acknowledge both short-term challenges and longer term trends that add some shading to this optimism.

Consumer businesses are, by nature, often low margin. That means that as the availability of investment has dried up, companies in this category have been particularly challenged by the global funding winter. With less access to capital, many have had to push hard for profitability. That’s led to the recent wave of layoffs and some closures. It has also led to resilience and creativity.

We’ve seen online stores like Edamama, an e-commerce platform for parents, and cloud kitchen player CloudEats, both from the Philippines, experimenting with offline locations in an effort to find other revenue. Indonesia, a predominantly Muslim country, has been working to position itself as a global hub for the halal industry, including food, cosmetics, and pharmaceuticals. The Malaysian halal Food industry was expected to grow to $113 billion by 2030.

While we believe there is still a lot of potential for growth in the B2C sector, that does not mean that Southeast Asia entrepreneurs will not eventually turn towards building B2B or deep tech companies as these ecosystems mature. Just as the first wave of Latin American startups built out digital infrastructure and services for consumers before turning to disrupting other sectors, Asian founders are likely to follow a similar pattern of looking to higher margin, economy-transforming industries over time.

In particular, we are already seeing signs of increasing interest in green tech across the region. In Indonesia, the number of disclosed investment deals in the sector tripled in 2022 compared to 2021. This is in line with the country’s target to achieve net-zero emissions by 2060. Malaysia has committed to increase renewable energy composition to 70% of total generation capacity by 2050, which is likely to drive interest in green tech there as well.

In ecosystems around the world downturns are inevitable, as is creative destruction followed by further innovation. But a close look at the numbers shows that Southeast Asia is well positioned to weather the current challenges and continue its consumer-led startup boom. We’re excited to invest in the next generation of founders building on the technology base laid down by previous startups and betting on the region’s dynamic, young, digitally-savvy consumers.