2021 Greek-Tech Ecosystem Insights & 2022 Predictions

Find more details on the protagonists of the Greek Tech scene and their impact on the transformation of the Greek market, inside our analysis.

This article originally appeared on Endeavor Greece’s website.

“There is an unrestrained optimism all around that puts you in a positive spin” this is the best way to describe what has been happening in Greece for the last few years. Long a top destination for travelers, Greek tourism revenue is on a roll for 2022 and forecast to pass that of 2019. Greece’s innovation sector, though less well known internationally, is expanding rapidly at the same time that the country is rediscovering its leadership voice on major world issues, including equality, democracy, and peace. Greece is stepping up and putting itself on the map.

Reborn as an emerging innovation hub after years of economic turmoil, Greece combines the energy of a nation determined to reimagine its future with the deepest of historical roots. In a world where there are no longer geographic limits on where top talent can work, countries that have strong brands as destinations can compete on quality of life, creating an unmissable opportunity for countries like Greece to become centers for tech and innovation communities and a home base for the next generation of leaders.

As Greece rebuilds and polishes its brand to compete with other rising hubs, it becomes increasingly open and connected. Greece already ranks among the top 10 destinations for migration by Ultra High Net Worth Individuals (UHNWI). Almost 1,200 millionaires are expected to move to Greece in 2022 alone. It is also seeing record amounts of Foreign Direct Investments hitting a 10-year record high in 2021 (up by an impressive 74.3% from 2020). We have a generation of Greek ScaleUps that are increasing their influence, size, and impact on the Greek Tech Ecosystem, they are building a new generation of executives and developers they are closing world-class deals: amongst them, Viva Wallet, Blueground, Skroutz, Workable, Beat, Hellas Direct, e-food, Epignosis, Instashop, Softomotive, Schoox, Spotawheel, Orfium, ActionIQ, Persado, Omilia, and Marine Traffic. Big Tech companies and foreign startups are also setting up a local presence in Greece. Giants like JP Morgan, Meta, Microsoft, Delivery Hero, Applied Materials, Samsung, and Prodege have all closed M&A deals with Greek startups over the last two years, and others like Cisco, Pfizer, TeamViewer, P&I, Microsoft have set up R&D and Innovations centers in Greece, At Endeavor we have mapped and are working with 85 foreign startups that have opened Greek offices, tapping into the great quality of local talent, a good cost to value ratio and the strategic location: amongst them Checkout.com GoStudent, and Panther Labs. Worldwide, there are 540 foreign startups with founders of Greek origin, including BetterUp, Jokr, Cameo, and Raise. Many of these companies are looking into connecting with Greece and/or opening offices in Greece in the coming years.

Why this report matters

Endeavor’s 2021 Greek-Tech Ecosystem Insights report is 100% run and validated by Greek entrepreneurs themselves. Every year we reach out to dozens of founders and ask them to share with us their growth numbers, milestones, and projections. Our goal with the Greek Tech Impact report is to generate an analysis that is entrepreneur-first, accurate, and which encapsulates the size and accomplishments of the broader Greek Tech Ecosystem in a way that highlights Greece’s proper place on the global map.

As a member of a global organization on a mission to build and support innovation ecosystems in secondary markets, Endeavor Greece has been working relentlessly for 10 years to put together a diverse, global, high-impact community of founders, talent, investors, and key stakeholders anywhere in the world that wants to be connected with the Greek tech scene. These audiences are Greeks in Greece, diaspora Greeks, and foreigners who have ties, teams, investments, or interests in Greece. We work with this unique, broad, diverse network to measure not just the accomplishments and traction of Greece-affiliated companies, but also spotlight opportunities for the Greek economy as well as design an extroverted, ambitious strategy for the Greek Innovation Ecosystem and Greece’s post-crisis transformation.

Panagiotis Karampinis

Managing Director, Endeavor Greece

Our approach

For this report, we collaborated directly with the founders that are leading the fastest growing companies in the country to capture in numbers what happened in the Greek ecosystem in 2021. Our analysis consists of a combination of publicly available information, Pitchbook Data as well as proprietary Endeavor data, while the vast majority of our information has been validated by the entrepreneurs themselves. For the needs of this report, we identify as “Greek Startups” all Greek-founded companies with more than 20% of their total teams based in Greece. We identify “Diaspora companies” the Greek-founded companies that have less than 20% of their total team based in Greece and we analyze their results in a separate section so that the homogeneity of the sample and the conclusions are preserved.

Key Insights

- 2021 was a record year for the Greek Tech scene. Fundraising hit a new full-year record, exceeding $1B in equity and debt raised by Greek startups, which represents an approximately 110% jump compared with 2020.

- The number of FTE employees at Greek startups and scale-ups grew by 82%, reaching the all-time high record of 12,785 full-time employees globally, 66% of which are based in Greece.

- 138 international companies in different stages, from startups to big-tech, have set up tech teams in Greece totaling 8650 employees in tech positions.

- Greek startups are becoming key drivers of job creation, as the total number of full-time jobs from startups in Greece (8536) is at parity with the full-time jobs created by the international tech companies that have a Greek presence (8650).

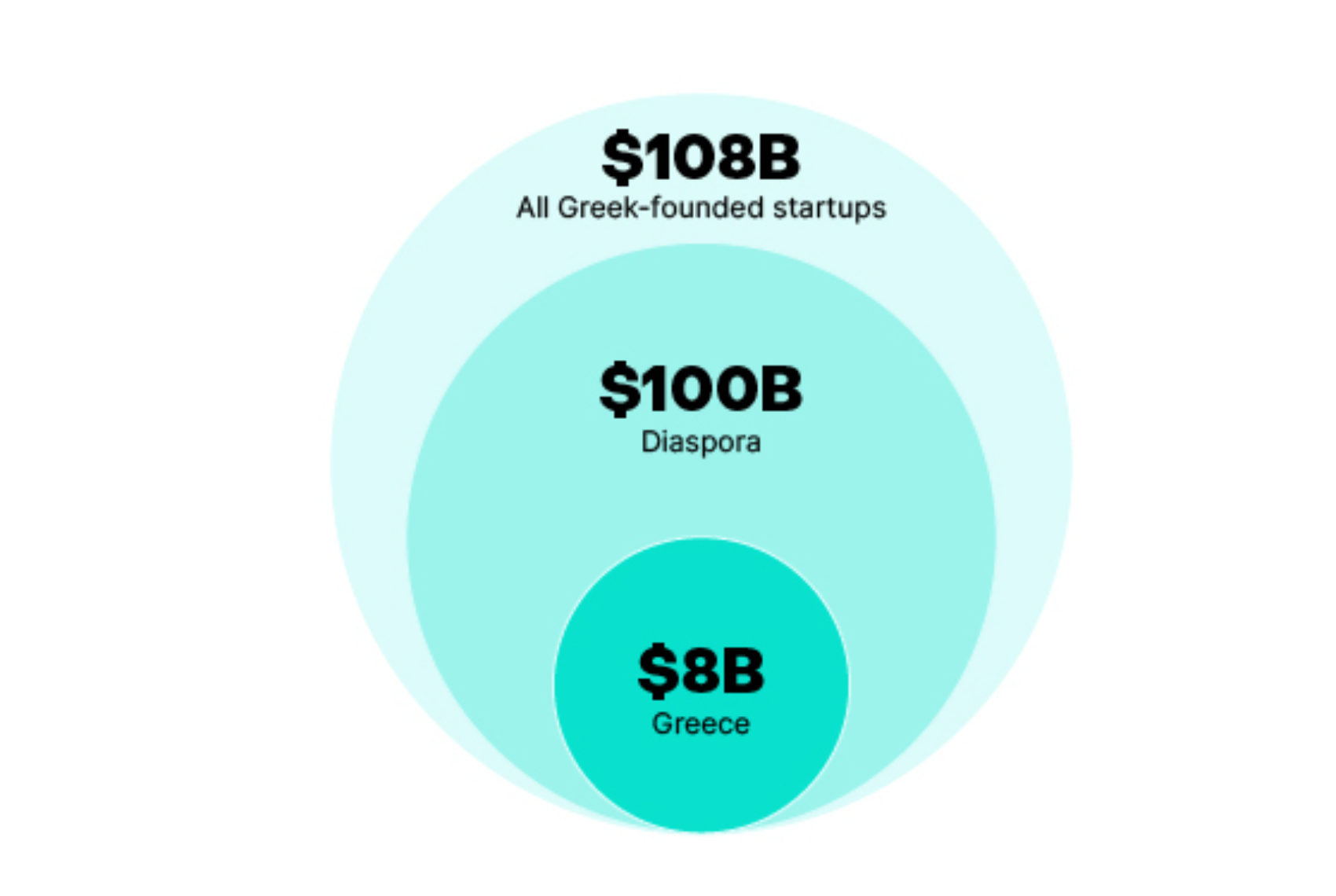

- Our research has mapped and is tracking 523 diaspora startups, whose value is estimated at more than $100B+, 13 times bigger than the total value of Greece-based startups which is estimated at approximately $8B.

- Greek diaspora startups raised a total of $6.8B in debt and equity in 2021, a number that is 6 times larger than the capital raised by Greece-based ones ($1B).

- Our research has identified 17 Greek-founded startups at Unicorn status (valued at more than $1B), 10 of which reached Unicorn status in 2021.

- 2022 started strong for the Greek ecosystem – only in the first half, we have seen the first-ever Greek-based Unicorn (Viva), $331.2M raised in debt and equity, and 11 mergers & acquisitions, so far.

- 2022 started strong for the Greek ecosystem and we saw what is likely to be the year’s biggest headline within the first 25 days of the year: Viva became the first-ever Greek-based startup to reach Unicorn status after a massive minority acquisition deal with JP Morgan valued the company at $2B.

- For 2022, we are expecting a 20-40% slow-down, compared to 2021 in capital raised by Greek startups in 2022 since during the first half of the year the invested amount has reached only 30% of the total amount invested in 2021

Investment Landscape

Fundraising hit a new full-year record in 2021, exceeding $1B in equity and debt financing, which is approximately 110% higher compared with 2020. Additionally, we notice a 30% increase in the number of funding rounds, from 65 in 2020 to 85 in 2021.

Taking a closer look at the financing amounts per vertical, we see an impressive increase in the funding of Fintech startups, representing more than 55% of the total capital invested in Greek startups during 2021, while the Payments, Banking, and Insurance sectors are in the spotlight. Consumer startups are following with approximately 25% of the total amount with PropTech & Automotive sectors being at the epicenter. Last but not least, Education & Talent startups are completing the Top3 funded verticals representing 8% of the total capital invested in 2021, with the Workforce and Lifelong Learning sectors having the largest contribution.

An interesting observation from the 2021 data, is that the largest percentage (almost 54%) of the total capital invested was channeled to Greek startups in the age group of 3-5 years old, in contrast to last year when the most mature startups (10+ years) led the chart, thus showing that more startups are approaching scale-up phase earlier in their lifetime.

The top 3 funded companies of 2021 were Storfund, which raised approximately $410M through a combination of debt and equity; Blueground follows with their Series C round of $180 million, through a combination of debt and equity as well, putting the company’s post valuation at $750M. Last but not least, Viva Wallet received $80M of development capital keeping its strong position in the top-funded companies in Greece for one more year.

Startups as a driver of new job creation

For yet another year, our research shows a significant increase in employees working at Greek startups and scale-ups, reaching the all-time-high record of 12,785 employees in 2021, compared to 7,000 employees in 2020, an increase that reached 82% totaling 5,785 new jobs created in 2021 by Greek startups.

Out of the 12,785 employees, 8,536 (approximately 66%) are based in Greece, while the rest are working from anywhere in the world, either in established offices of the companies abroad or remotely. Narrowing down the focus to new jobs that were created for Greece-based talent only, we still notice exceptional growth that reached 36%, totaling 2,304 new jobs created in 2021.

A more detailed look at the growth of employees in startups by sector in 2021 shows that Commerce has a very strong contribution to job creation for the second year in a row, showing annual growth of 43% compared to 2020. Business Process Management, Cloud Computing, Marketing, and Automotive sectors are completing the Top 5 list of drivers in job creation for the past year. An important change in 2021 is that we see the Travel & Hospitality sector back on track after a significant decrease in employees during 2020 due to the impact of the pandemic.

The companies featured below rank the highest in the list of top employers based on their number of employees in Greece.

An interesting notice of this year’s research is that the top 20 startup employers are occupying less than 50% of the total employees, while last year the same percentage was close to 63%. This fact shows that there are more early-stage companies rapidly growing their teams, thus talent is being equally split between larger and smaller startup employers.

From both sides, the fastest-growing startups are the ones leading the job creation We divided the fastest-growing employers into two categories, the ones that have crossed the line of 50 employees which we consider to be a crucial point towards scaling, and the ones that are showing high-growth signs at an earlier stage. Both lists are given in alphabetical order.

Greece as a “nest” for tech talent

In the last few years, we have seen a dynamic trend of foreign tech companies of any size, from startups to big tech giants, building research and/or technology hubs in Greece. In this section, we tried to capture the current state of this trend, using this report as the starting point for tracking the creation and progress of international companies building tech teams in Greece to understand the value they bring to the local ecosystem.

Our research identified 138 international companies that have established a tech hub in Greece, out of which 73 are multinational companies representing 18 countries and employing more than 8000 people in tech positions.

If we take a closer look at the multinational companies list, we notice that the top10 companies that employ the biggest percentage of employees in tech positions compared to their total number of employees in Greece are Openbet (86%), Atos (81%), Citrix (78%), Nokia (75%), Accenture (63%), Ericsson(53%), IBM(51%), Microsoft(46%), Oracle (40%), Pfizer(32%).

The remaining 65 companies in the list fall under the categories of startups and scale-ups coming from 13 countries, totaling approximately 650 employees. Although the total number of employees might seem small, the presence of foreign startups in Greece is equally significant as it contributes directly to the extroversion of the Greek Tech Ecosystem and can potentially lead to increased attention from international investors and provide access to more resources for the overall ecosystem growth.

Out of the 65 companies listed in the startup/scale-up category, our research identified 12 with the largest teams in Greece, taking into consideration the number of employees in tech positions but also the percentage of employees in tech positions compared to the total number of employees. These companies are Sitecore, Toptal, Indeavor, Global Web Index, Capture One, Sunlight.io, Rokoko, Adzuna, Fairlo, Axiomatics, Intuition Robotics, and Panther.

Although the reasons to start a team in Greece vary from case to case, we have identified some common factors that are affecting the decision of building and growing it. The first and most important factor is the number of graduates from tech-related departments, such as the big pool of engineering talent in Ioannina that led big companies like TeamViewer and P&I, but also the scale-up BestSecret to establish their tech team in Greece. Another factor that is also attached to the country’s higher education is the tech departments that are building specializations like the one of hardware engineers in Heraklion, which led the startup Sunlight.io to build and grow the biggest part of its team globally in Greece. Last but not least, the continuously growing startup landscape and the increased acquisition activity that has been noticed in the last few years is also a crucial factor for international companies maintaining and growing their tech teams in Greece. Some good examples of this aspect would be the acquisitions of Moosend by Sitecore in 2021 and Blendo by RudderStack in 2020.

Looking ahead, we see the presence of more international companies of any size as more than positive and crucial for the overall development of the Greek tech ecosystem. Specifically, we are expecting all these companies to have a significant contribution to the creation of tech jobs in the country, while at the same time the Greek tech ecosystem benefits from the wide range of international opportunities to attract back some bright minds that are currently working abroad.

The Diaspora Opportunity

By definition, a startup ecosystem consists of a group of people, startups, and related organizations that work as a system to create and scale new startups. The Greek ecosystem goes far beyond the geographical boundaries of the country, given the great opportunities that come from the Diaspora Greeks: extended access to capital, talent, strategic advice & insights from the global innovation landscape, and other resources.

Greek-founded startups that are located in any part of the world also represent a unique extroversion opportunity for the local ecosystem. For the purposes of this report, with the term “diaspora startups” we will be referring to any Greek-founded company that has less than 20% of the team located in Greece or no operational connection with Greece at all.

Our research identified 523 diaspora startups whose value, according to our estimations, surpasses the amount of $100B. This number is 13 times bigger than the total value of the Greece-based startups which we estimate to be totaling $8B. While we might have missed some cases, we are confident that this is the closest to accurate estimation to date.

Indicatively, the 10 most valued Diaspora Startups based on publicly available information on most recent valuations are the following:

Greek diaspora startups raised in total $6.8B in 2021 both in Equity & Debt Rounds, a number that is 6 times larger than the capital raised by Greece-based ones ($1B). More than 72% of this amount was allocated to Growth Stage Rounds (Series B+).

Diving further into the investment activity for diaspora startups, we came up with the list of the Top 10 funded companies of 2021. The ranking includes the total amount of all funding rounds per company that took place during the year.

Following the large funding rounds of 2021, 10 diaspora startups hit unicorn status in 2021, while our research has identified in total 17 Greek-founded startups that are valued at more than $1B, the majority of them being in the Healthcare, Fintech, and Consumer spaces.

2022 so far & our predictions for the year

As we are getting closer to the first half of the year, it is clear that 2022 has started strong and we have already noticed significant highlights in the progress of the Greek ecosystem. The headlines for 2022 were made in just the first 25 days of the year. Viva Wallet’s deal with the American banking giant JP Morgan which acquired 49% of the company, turned Viva Wallet into the first Greek unicorn marking a very important milestone for the Greek tech scene and a record valuation that will be very tough to break over the next 11 months. The impact of the Viva Wallet deal was massive as the news attracted global attention and the deal itself became a flagship for what is the Greek Tech momentum. A sizable deal, and a vote of confidence that cannot be ignored, a game-changer for the Greek scene.

Additionally to Viva Wallet’s valuation which has a significant contribution to the total value of the Greek-tech ecosystem ($8B), we provide a list of the 10 highest valued startups based on announced valuations and/or Endeavor estimations.

Furthermore, 11 more mergers and acquisitions have already been completed during 2022 whose value surpasses the $250M based on market estimations, while approximately 80-90% of the total value is coming from the top 3 acquisitions (given in alphabetical order):

- Accusonus, a company that builds next-generation audio repair and music creation software, got acquired by Meta – Facebook’s parent company.

- Pollfish, an agile market research platform offering real-time responses from mobile consumers got acquired by Prodege, a cutting-edge marketing, and consumer insights platform out of California.

- Transifex, a Localization Automation Platform that helps developers and marketers publish digital content across multiple languages got acquired by PARC Partners, a US investment firm.

The full list of acquisitions completed in 2022, in alphabetical order:

In closing, a very positive notice from our 2021 analysis is that the growth of the ecosystem is split equally among growth and earlier stage startups (rising stars). Following, we provide a shortlist of startups that we are watching and have strong indications that will be in the spotlight in 2022 by making big headlines and/or having a significant contribution to the 2022 aggregated ecosystem metrics.

Companies to watch in 2022

The 2022 macro perspectives from our mentors

At Endeavor, we host hundreds of mentoring sessions, panel discussions, thought-leadership conversations around the world. These are a great resource for market insights and we have consolidated a few of the most important points we have heard so far.

Despite this strong start to the year, it is clear that the ecosystem is facing interlocking global crises that have stunned the world with their velocity and impact. Disruptions in the value chain, out-of-control inflation, the Ukrainian war and geopolitical instability that it caused, and the energy crisis are all problems that either did not exist or did not cause much concern in the first days of 2022. By most metrics, it is too soon to understand their full impact, but from what we are seeing so far, there has already been a steep drop (30-40%) in new growth rounds and the post-money valuations offered have dropped by 60-70% in most major industries in the US. In different panel discussions and sessions that we host at Endeavor worldwide, we see that the majority of investors do not believe the correction is transitory, with the vast majority expecting the current cycle to continue for at least 24 months. Almost half of the investors expect that the worst is yet to come.

The disconnect between private and public markets is also likely to affect how investors assess opportunities going forward. Publicly traded companies have far more attractive valuations based on revenue multiples and that is expected to drive more investments in the public markets and perhaps slow down a bit their investments in venture capital and private equity funds.

From “growth at all costs” to “survive to thrive,” the emphasis at most private companies is shifting from burning cash to conserving capital and reaching profitability. Capital-intensive deep tech companies will struggle in the short to medium term. The ones who have raised a lot of money will try to make it last longer than originally expected. While multiples have come way down from recent highs, they are still not particularly low by long-term historical standards, so theoretically they can drop further. That being said, the “micro” side of the economy is not the major concern right now. It is the “macro” piece of the equation (geopolitics, inflation, energy and supply chain costs, etc.) that is primarily affecting markets. Therefore, if the macro picture improves, we could see a faster recovery than the typical 3-4 years it generally takes to go from boom to bust.

Conclusions for Greece

For the Greek tech ecosystem, we are expecting a 20-40% slow-down in capital raised by startups in 2022 given that, during the first half of the year, the total amount invested has barely reached 30% of the total amount invested in 2021.

Overall, we still have a long way to go and the future of the global economy looks uncertain at best, a reality that will definitely slow the growth of the Greek Innovation Ecosystem. Despite our optimism about the future, Greece remains near the bottom of the European Commission’s 2021 Digital Economy and Society Index, scoring low on connectivity, internet use, and digital public services. We face stiff competition from other southern European tech hubs like Portugal, which hosts Europe’s biggest technology conference, Web Summit. For the Greek Innovation Ecosystem to achieve the much-needed further growth, we need to bring more extroversion and a think-bigger mentality into the ecosystem. Attracting international talent and more international investments, hosting more international and regional projects, events and initiatives, connecting with foreign innovation ecosystems in a more meaningful way, actively promoting Greece as a destination for innovation, and expanding our national narrative

In setting the goals for 2030, we believe that the Greek Tech ecosystem should be able to produce 10 unicorns by 2030. By December 2022, Endeavor Greece will work towards publishing a 2030 Innovation Plan as an effort to formally set forth our long-term goals of how we will continue to support the Greek Tech Ecosystem to help it achieve that number.

Featured Stories

AI isn’t confined by geography; capital is. Let’s shift the map.

New Zealand is known for its landscapes, not its founders. That is why Endeavor is launching there.

2024 Endeavor Impact Report: Building a New Global Home

Related Articles

AI isn’t confined by geography; capital is. Let’s shift the map.

New Zealand is known for its landscapes, not its founders. That is why Endeavor is launching there.