2024 Endeavor Catalyst Annual Report:

A Look into Global Venture Capital

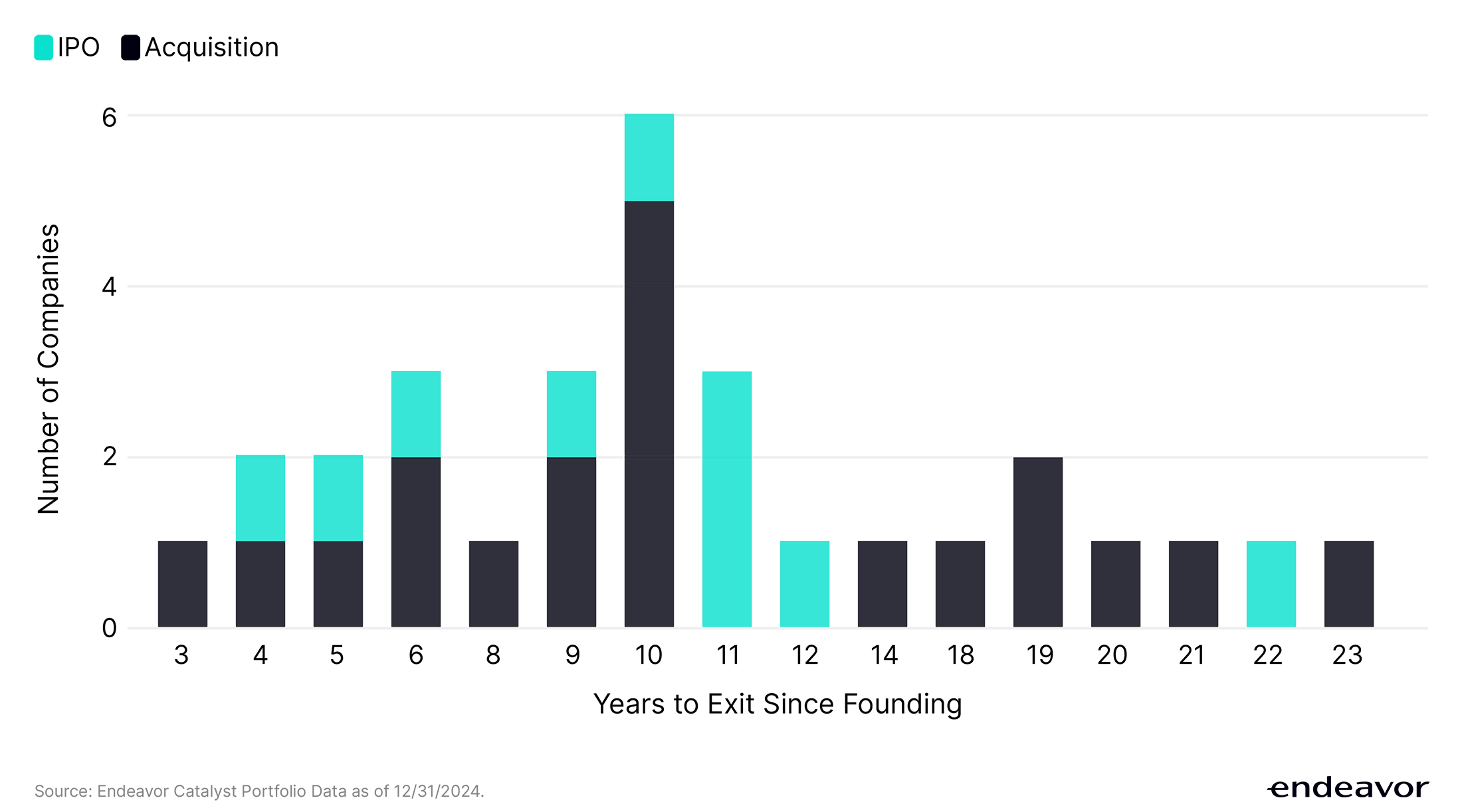

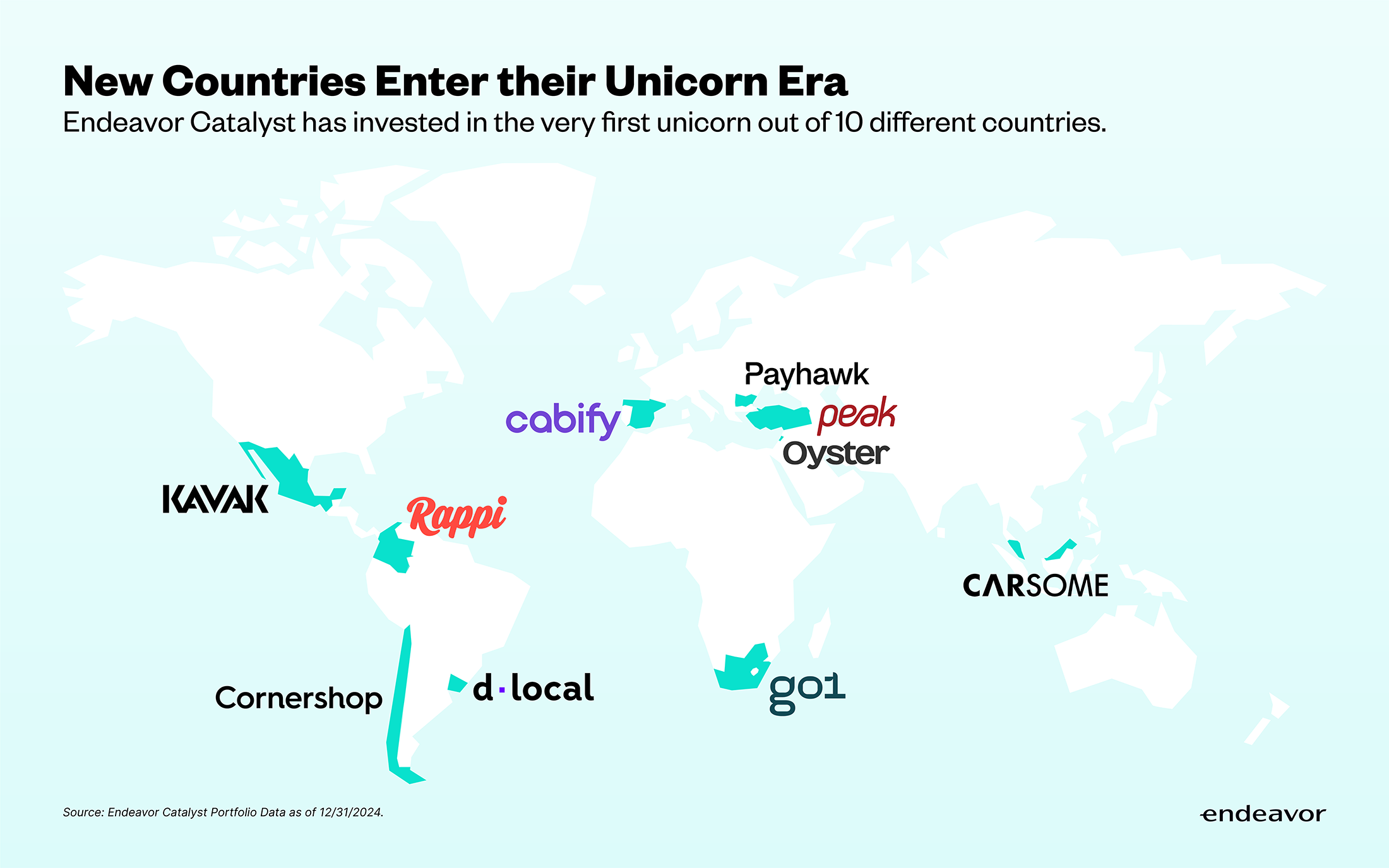

All information in this report is as of 12/31/24, unless otherwise noted.

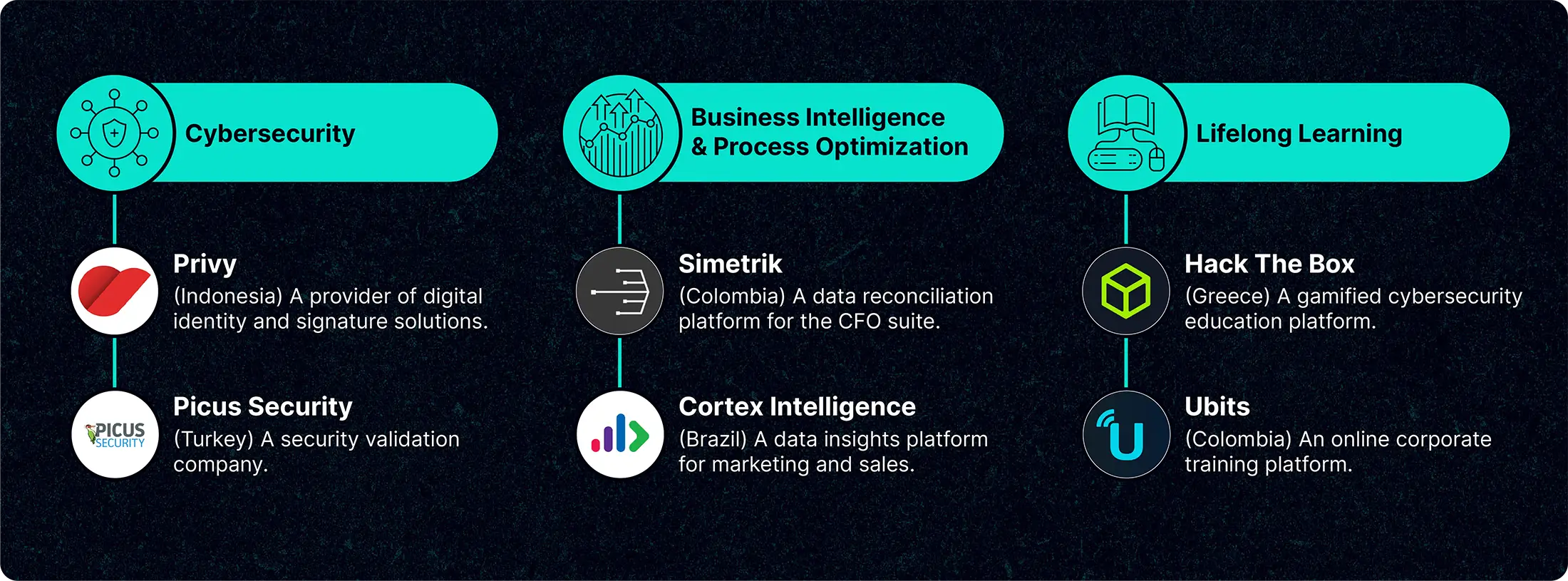

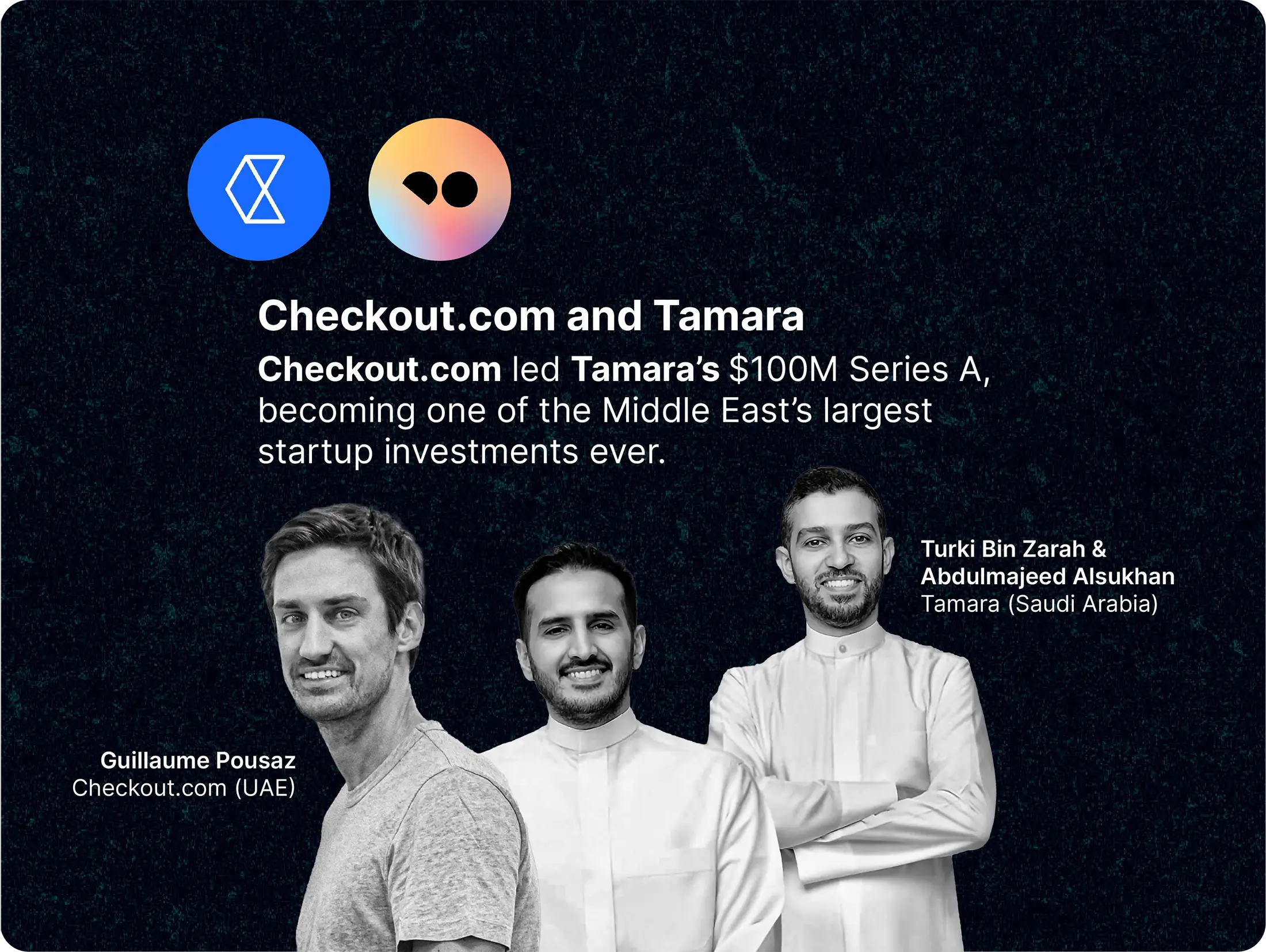

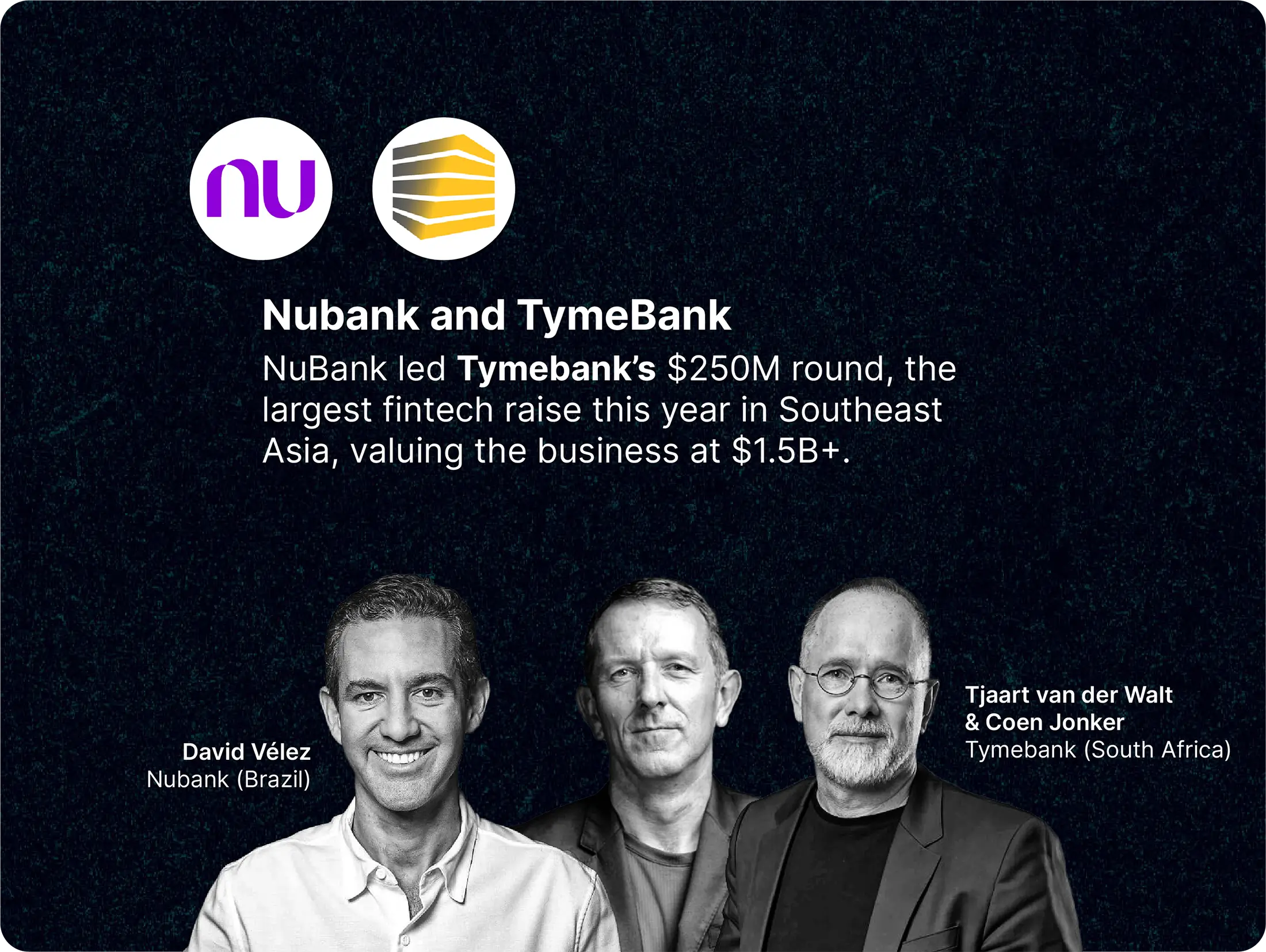

All bolded companies mentioned are part of the Endeavor Catalyst portfolio.

All bolded companies mentioned are part of the Endeavor Catalyst portfolio.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}