Global venture capital experienced a significant pullback in 2023. In reality, it was a return to normal. Media headlines brought attention to the decrease in investment volume, valuations, and check sizes, but these numbers closely aligned with pre-2020 levels.

Early stage investing proved especially resilient, and the entire venture capital market showed renewed optimism in the second half of the year, particularly in frontier industries (think: AI). A hint of lower interest rates and strong equity markets helped paint a rosier picture. Will this optimism translate into increased investment activity in 2024? Only time will tell, but it certainly feels like the worst may be behind us.

Although global markets continue to reflect a higher level of economic and geopolitical uncertainty, GPs and LPs alike are emphasizing the importance of staying invested, hoping to avoid suffering vintage-year holes in their portfolios this time around — a lesson learned from 2001 and 2008. The old adage, “it’s not about timing the market, but about time in the market,” has repeatedly proven true over the years in public and private markets alike.

“At Endeavor Catalyst, we are steadfast in our belief of the power of entrepreneurship — investing through cycles and staying in markets where and when many are retreating. We are reminded that these challenging conditions are in fact table stakes in our markets, highlighting the grit and resilience of our Endeavor Entrepreneurs, and why we have and will continue to bet on them.”

What We’re Seeing:

Return to First Principles

Capital efficiency and profitable business models are once again a top priority for founders and investors alike, especially as they consider new priced equity rounds.

Valuation Resets

Down rounds climbed to a 10-year high at 17% in Q3 2023, a number that has trended upward for several quarters. This is due in large part to elevated valuations in 2021/2022.

Alternative

Financing Options

With a higher bar for raising new priced equity “up” rounds, we are seeing an increase in insider-led, bridge and extension rounds, SAFEs, convertible notes, and venture debt.

The

AI-First Era

AI is at a critical inflection point and ripe for innovation and commercialization. AI companies globally are capturing significant venture dollars in a dim funding environment.

Failure Is an Option

Many companies have failed to successfully monetize their business and/or raise capital to fund operations. While startup failure rates are already historically high, they’re trending even higher.

Significant Dry Powder

Venture and private equity funds are sitting on significant dry powder. While much has been directed toward existing portfolio companies in 2023, appetite for new investments is increasing.

Great Companies Always Prevail

Entrepreneurs are resilient and seek to capitalize on all opportunities, including opportunistic mergers and acquisitions (M&A). Some of the most exciting and generation-defining startups have been built in the toughest of times.

Selectively Open

Public Markets

The IPO market is selectively open for companies with clear growth, profitability, and reasonable valuations. Underperforming publicly traded companies are reevaluating their future (e.g. public to private deals, bankruptcies, and Chapter 11 filings).

Our Unique (Global) View

In just over a decade, we’ve raised half a billion dollars across four funds and invested in 300+ companies from 37 markets around the world, helping to advance Endeavor’s mission to build thriving entrepreneurial ecosystems globally. From day one, we aimed to create a dependable income source to sustainably fund our nonprofit mission, and enhance it by financially supporting Endeavor Entrepreneurs and generating returns (and awareness of emerging markets) to LPs.

Endeavor Catalyst at a Glance

0+

Years of Operation

0

Investments

0

Markets

$ 0 M+

Assets Under Management

0

Exits

0

Companies valued at $1B+

0

Publicly-listed Companies

0 +

Co-investment Partners

A History of VC in Emerging Markets

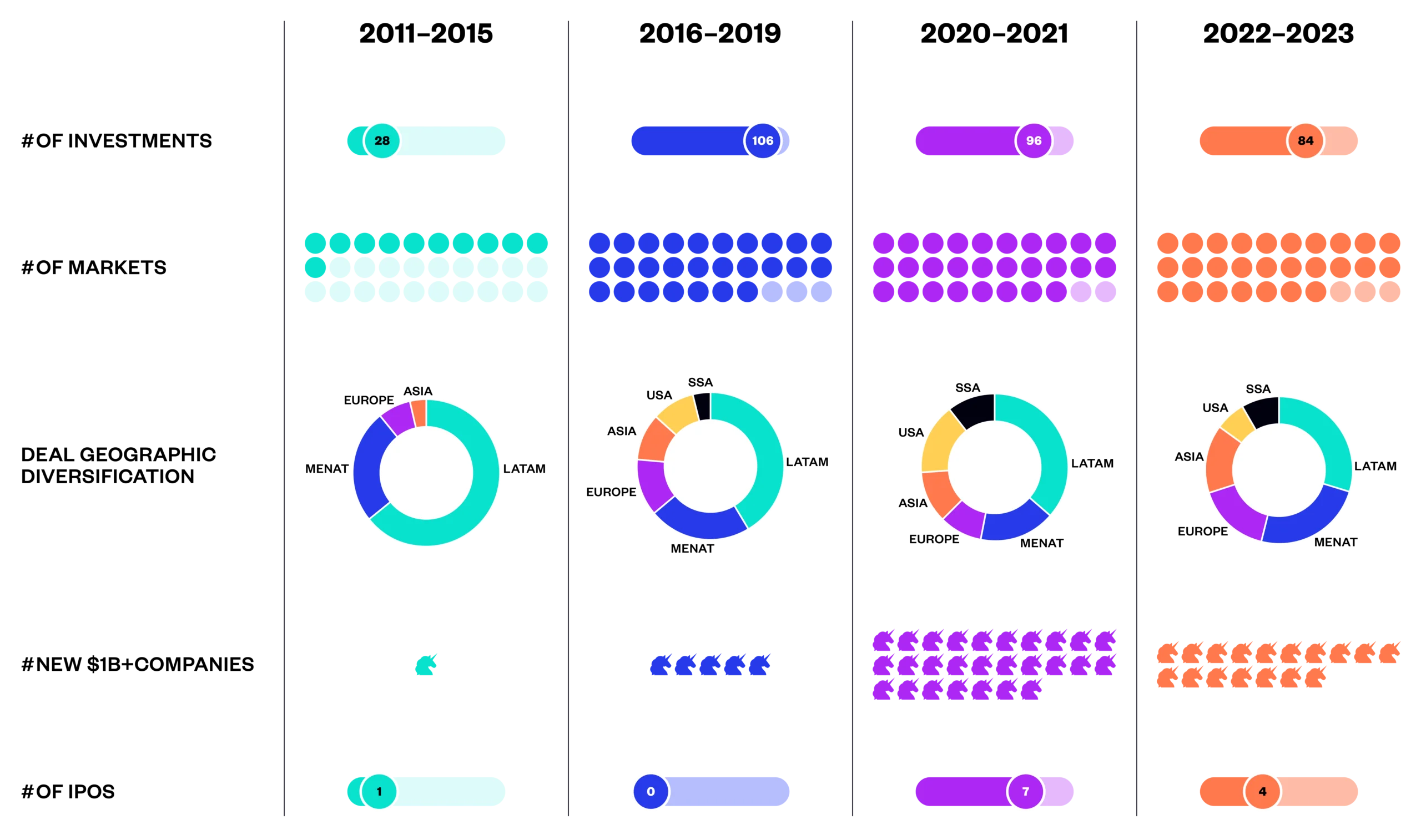

Venture capital is defined by its cycles, and we’ve experienced quite a few in the 42 worldwide markets Endeavor has operated in over the past 12 years.

Early players entered emerging markets during this period, fostering venture capital as an asset class and seeding local entrepreneurial ecosystems. Both capital and deal flow was finite, but early commerce and consumer-led companies emerged, attracting regional attention.

As these early venture-backed companies grew, so did their capital needs. International venture funds and crossover funds — with the ability to write larger checks — landed in these markets for the first time. Technology trends also shifted toward building financial solutions.

The global pandemic accelerated digital adoption, creating significant opportunities in emerging markets. As companies jumped on the opportunity to solve these real-world problems, capital followed — chasing yield in a record low interest rate environment. While many technology-enabled industries benefited from these tailwinds, B2B services gained significant traction. Large injections of capital into the global economy — and increased consumer spending — caused inflation to spike.

Inflation concerns kicked off a chain reaction of interest rate hikes and a more sober dealmaking environment. With capital harder to come by, founders were urged to focus on profitability vs. growth at all costs and extend runway. Meanwhile, investors primarily focused on their existing portfolios and less risky assets. Though these effects were felt globally, they were especially painful in emerging markets.

Early players entered emerging markets during this period, fostering venture capital as an asset class and seeding local entrepreneurial ecosystems. Both capital and deal flow was finite, but early commerce and consumer-led companies emerged, attracting regional attention.

As these early venture-backed companies grew, so did their capital needs. International venture funds and crossover funds — with the ability to write larger checks — landed in these markets for the first time. Technology trends also shifted toward building financial solutions.

The global pandemic accelerated digital adoption, creating significant opportunities in emerging markets. As companies jumped on the opportunity to solve these real-world problems, capital followed — chasing yield in a record low interest rate environment. While many technology-enabled industries benefited from these tailwinds, B2B services gained significant traction. Large injections of capital into the global economy — and increased consumer spending — caused inflation to spike.

Inflation concerns kicked off a chain reaction of interest rate hikes and a more sober dealmaking environment. With capital harder to come by, founders were urged to focus on profitability vs. growth at all costs and extend runway. Meanwhile, investors primarily focused on their existing portfolios and less risky assets. Though these effects were felt globally, they were especially painful in emerging markets.

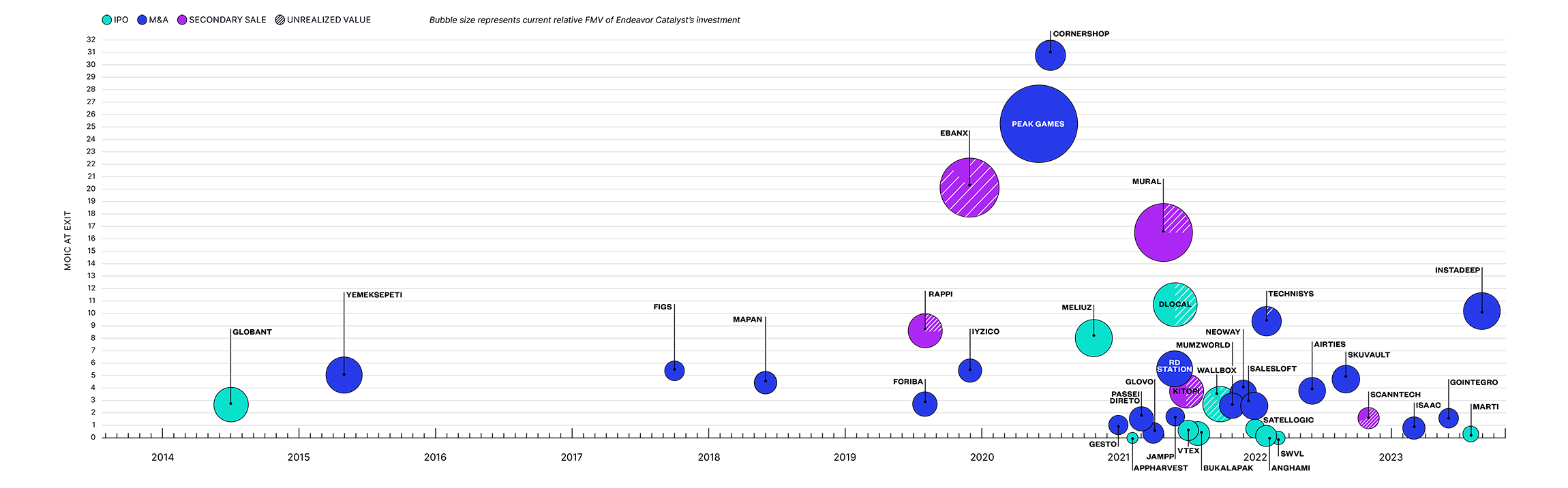

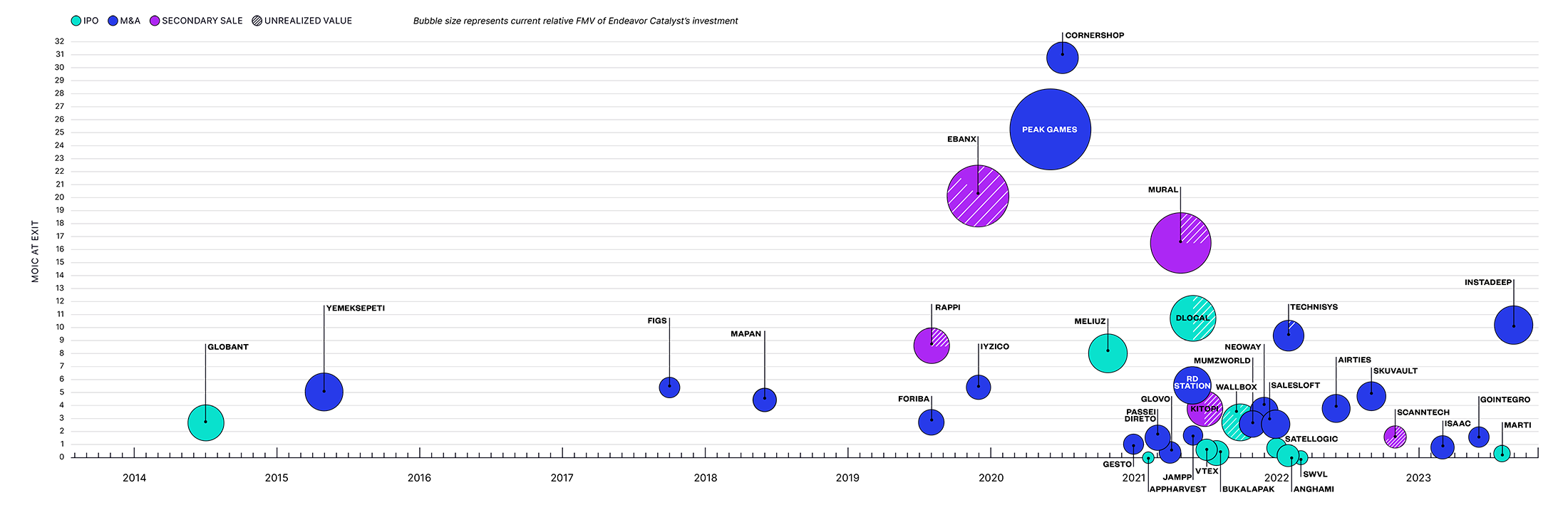

What does this look like in our own portfolio? Despite fluctuating sentiment around investing in emerging markets, we’ve leaned in — always believing in the long term potential of these markets. And it’s paid off.

Figure 1: Our History in Emerging Markets

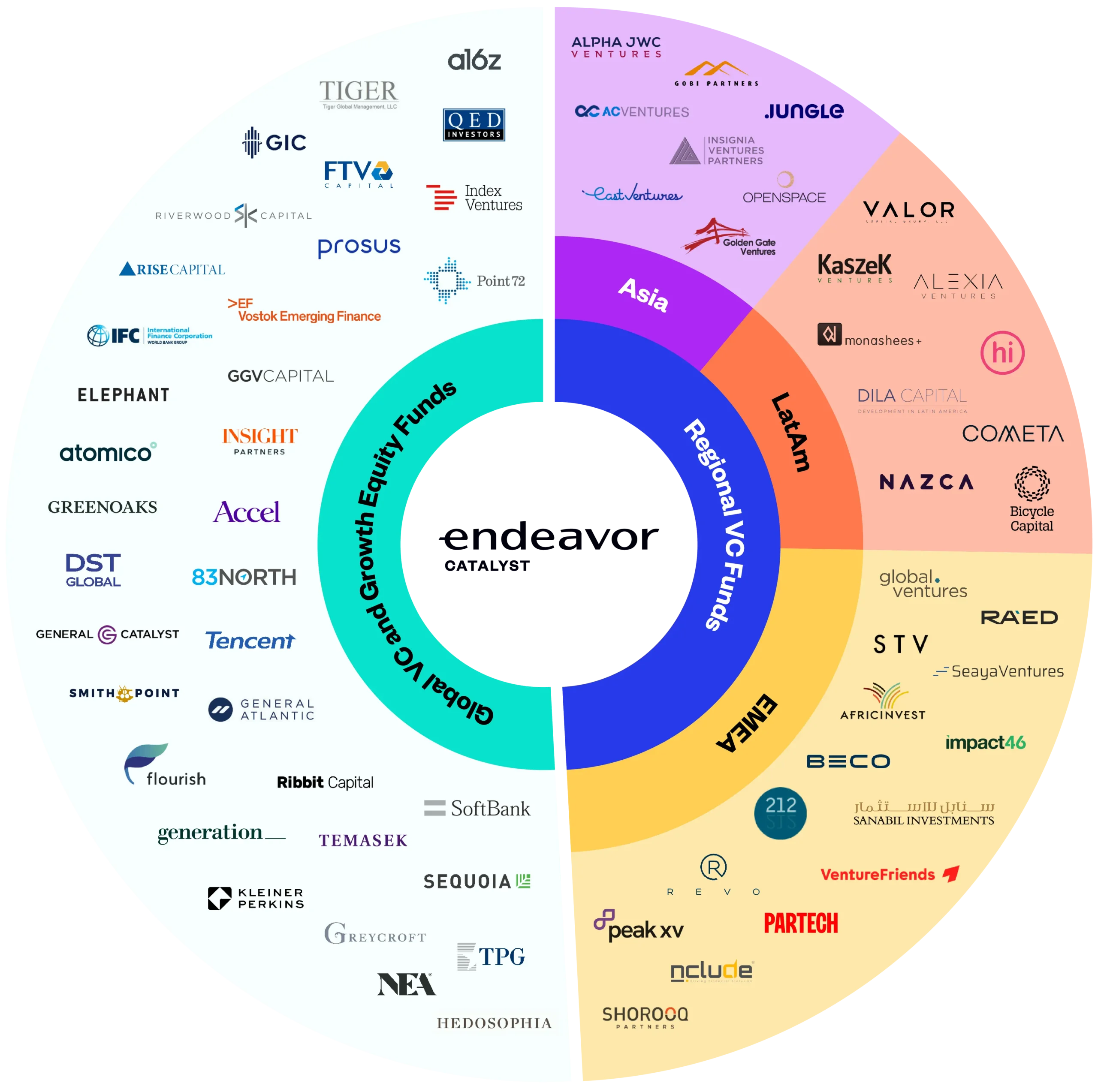

Top Investors Eye Emerging Markets

In 2021/2022, we watched global investors flock to emerging markets, and in 2023, we watched many of them fly away, but this time they left aware of the possibilities. Emerging economies are full of unique opportunities, with innovative startups and courageous founders leading the way. As more local companies solve global problems and achieve multiples and exits once reserved only for Silicon Valley, investors everywhere will take notice.

While many emerging markets now have strong, locally-focused, early-stage investors, they have historically lacked local funders willing to write larger checks at later stages — resulting in a dangerous funding gap for startups. (Our study of the Venture Landscape in Spain illustrates this gap.) This is changing with the entrance of new growth stage funds focused on Latin America, Southeast Asia, and Sub-Saharan Africa. We view a full stack of capital providers as an exciting sign of maturity and future growth potential in these markets.

Allen Taylor Managing Partner Endeavor Catalyst

“At Endeavor Catalyst we hold a high bar for co-investment partners, and we’ve seen qualified institutional investors emerge and build track records across the globe. It’s exciting to see others recognize the opportunity that exists in these markets.”

Figure 2: Our Most Active Co-Investors

VC Activity Returns to Pre-Pandemic Levels

In line with global trends, Endeavor experienced a significant pullback in venture funding in 2023 — following the funding frenzy in 2021/2022. However, we have seen investment activity trend upward for the past three quarters, eventually realigning with pre-pandemic deployment levels. (See Figures 3 and 4 below.)

In 2022, over 700 funds raised a record $160+ billion in fresh capital. This followed 2021’s venture fundraising record of $150+ billion. With significant capital raised during this period, and little deployed in 2023, there is plenty of dry powder going into 2024.

Looking ahead, we plan to remain patient and maintain a long term strategic outlook. While we do not anticipate reaching 2021/2022 funding levels anytime soon, venture capital in emerging markets has significant upside potential, and we expect to see sustained growth in the years ahead.

Round Size and Valuations Hit Reset

The correction in venture capital was not felt evenly across stages. Investors continued investing in smaller, early-stage companies at a consistent rate, but hid their checkbooks during late-stage funding rounds, cratering the segment as they insulated themselves from economic and short-term liquidity uncertainties.

The median pre-money valuation for Series A rounds we participated in was fairly resilient, decreasing 16% YoY in 2023 to ~$68 million. The median pre-money valuation of high-growth, late-stage company rounds we participated in (Series D+), however, fell 77% YoY to roughly $250 million. At later stages, many investors exited the asset class entirely, and the investors who remain are far more cautious — less willing to pay high revenue multiples for unprofitable companies. (See Figures 5 and 6 below.)

These effects have been felt to varying degrees across the globe. Within our own portfolio, Africa and Europe saw the largest drops in median pre-money valuations YoY (92% and 72% respectively), while MENAT proved to be the most resilient region (down 16%), largely due to strong government support. Asia and LATAM each saw ~50% decreases in their median pre-money valuations YoY. (See Figure 7 below.)

Shu Nyatta Founder and Managing Partner, Bicycle and Board Member, Endeavor Global

“There’s this interesting idea that [public and private] markets are totally different,” says Shu. “But it doesn’t make any sense to me that the private market can’t move up and down in the same way that the public markets do.”

In an effort to minimize dilution, falling valuations have led to smaller round sizes across stages and globally. Median round sizes in our portfolio decreased 60% from 2022 to 2023, and total capital raised went from $4 billion in 2022 to just $1 billion in 2023. (See Figure 8 below.)

When the market turned in H2 2022, startups were warned: preserve cash, extend runway, and attain profitability. Many did. However, cash can only last so long and many companies are beginning to approach the market. With their previous marks hovering at 2021/2022 peak levels, many companies may face flat or down rounds this year. In Q3 2023, down rounds accounted for nearly 20% of all global venture investing rounds, compared to just 5% in 2021. And they’re trending upward. While not aspirational, one could argue down rounds are a normal feature of a healthy private market.

Local Startups Bring Global Gains

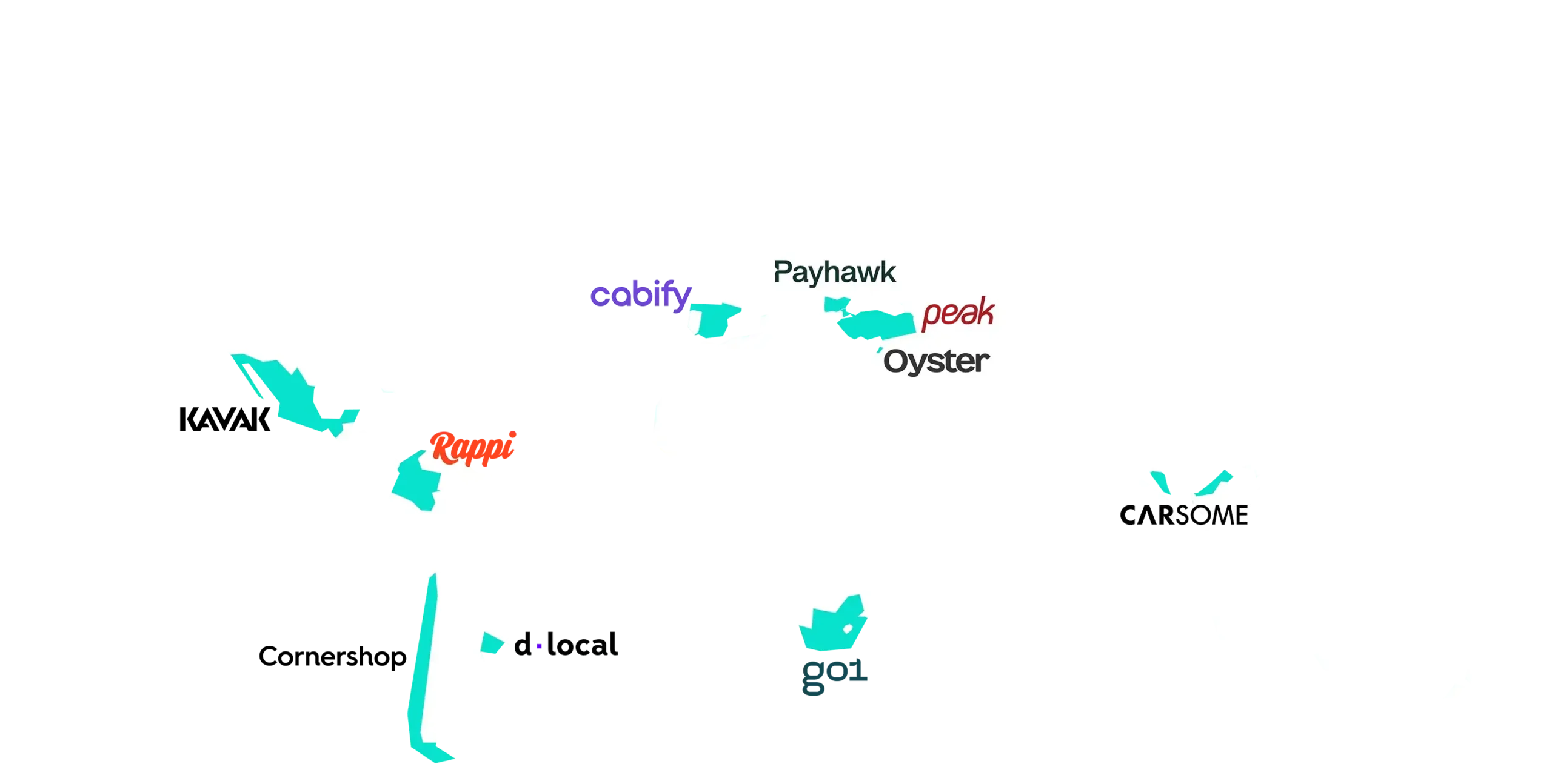

The Endeavor model has proven that high-performing companies can originate anywhere in the world. In our portfolio alone, we have 51 unicorns hailing from 22 markets. In 11 instances, we have invested in the very first unicorn ($1B+ company) from a market including South Africa, Bulgaria, Malaysia and Chile.

Figure 9: Global First Time Unicorns in our Portfolio

A decade ago, two thirds of all venture capital was raised by startups headquartered in the United States. Today, more than half of startup investments are raised by companies outside the US, and Endeavor Catalyst has had a front row seat to this shift. (See Figure 10 below.)

Emerging markets remain less competitive than the US, China, and India, and they have huge potential upside. The next big global fintech company could easily start in Uruguay (e.g. dLocal), or any other emerging economy. In today’s market, regardless of where they are founded — or where employees are based — companies can scale to solve global problems and service customers worldwide. A few examples include Oyster HR, a Lebanese unicorn that runs an employment platform that helps companies hire quickly and compliantly in ~180 countries, and Rocket.Chat, a young Brazilian open-source communications platform that already has millions of users in ~150 countries.

Figure 10: Regional Diversification Over Time

We have become increasingly globally diversified over time as Endeavor expands to 42 markets, though LATAM continues to be our largest market.

Tip: Filter the chart by tapping on elements in the legend; hover over bars and lines for detailed information.

Historically, Latin America (LATAM) has been our most active market — led by Brazil, which represents 16% of our portfolio. In 2021, Mexico and Colombia also began capturing significant dollars in the region, helping LATAM become the world’s fastest-growing region for venture funding.

Since 2022, our investment activity in the Middle East, North Africa, and Turkey (MENAT) region has accelerated, fueled by investments in Egypt and Saudi Arabia. Egypt’s venture activity has grown consistently over the past 5 years, and Saudi has benefited from exciting government initiatives launched to stimulate entrepreneurship and venture capital. Our investment activity in the US, Africa, Southeast Asia, and Europe also continues to grow, on pace with Endeavor’s expanding presence in these markets. (See Figure 11 below.)

We’re In It for the Long Haul

Venture capital is a boom and bust business — it’s cyclical, prone to hype and herd mentality, and hard to predict. It’s also the lifeblood of entrepreneurial ecosystems. Venture capital handsomely rewards independent thinkers, patience and persistence, and those willing to take the risks. This is true for investors and founders everywhere, and even more so in emerging markets where venture capital and entrepreneurship are particularly volatile.

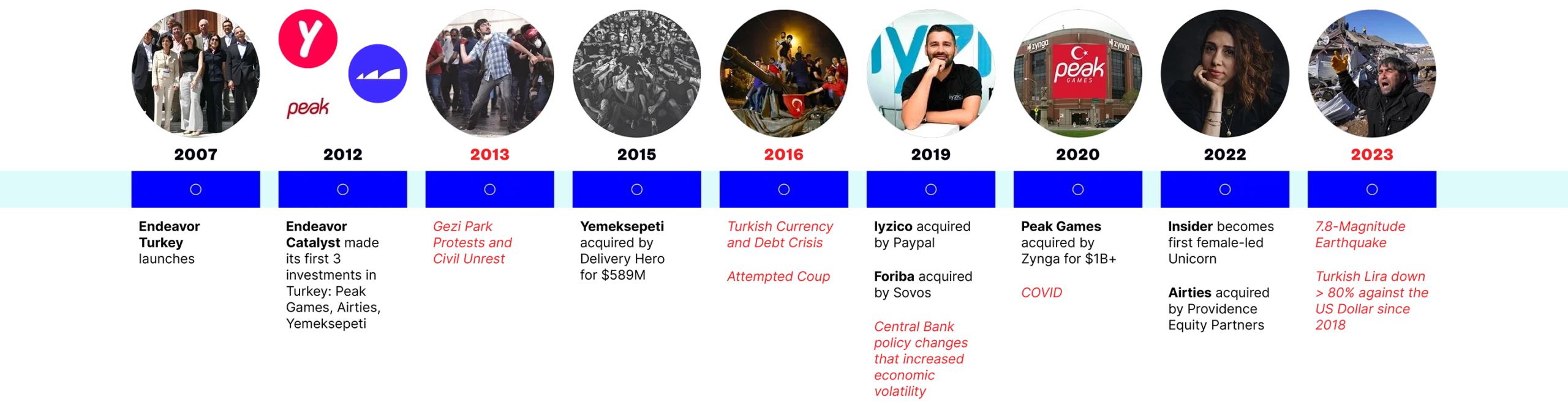

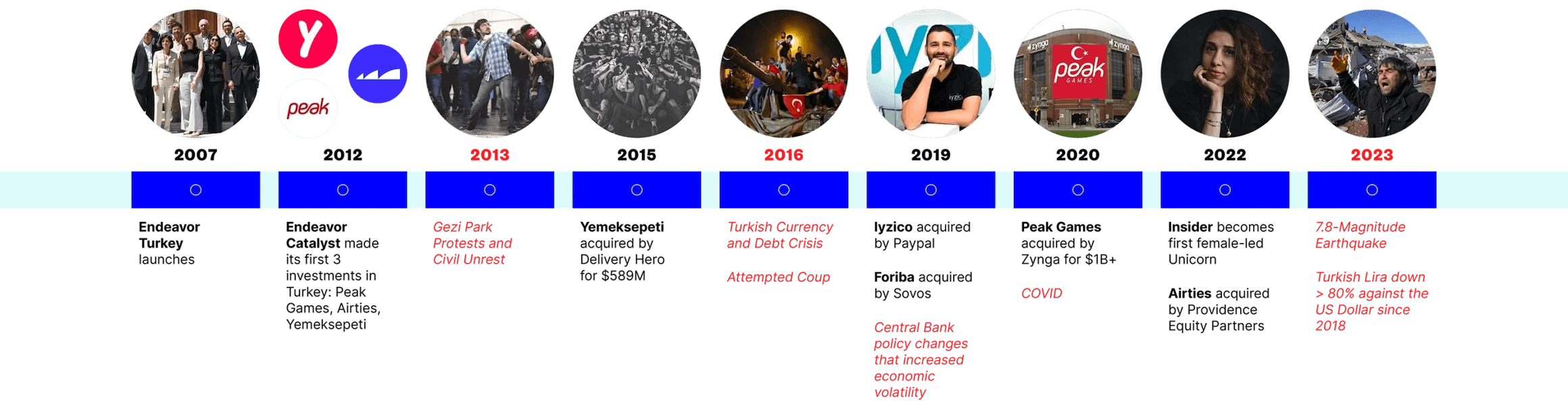

As an example, we’ll spotlight our success in Turkey. We made our first investments in the country in 2012 (Peak Games, AirTies, Yemeksepeti). When Asli Kurul Türkmen, Managing Director of Endeavor Turkey, was asked to summarize “the key macro events that went wrong” over the 10 years that followed, she answered: “basically everything short of a giant asteroid crashing down.” Jokes aside, the country was mired with social and political unrest, economic turmoil, and even natural disasters. Despite some of our co-investors retreating from the country, we stayed the course and doubled down, making 11 additional investments over this time period.

Over a decade later, Turkey is our top performing market across all of our funds. And those three early investments? Peak Games was acquired by Zynga in June 2020 for $1.8 billion, AirTies was acquired by Providence Equity in April 2022 for an undisclosed amount, and Yemeksepeti was acquired by DeliveryHero in May 2015 for ~$600 million. In spite of its challenges — or perhaps because of them — Turkey is a thriving entrepreneurial ecosystem that has produced six companies valued at $1+ billion — persistence beats resistance.

Figure 12: Endeavor in Turkey

Above we highlight some of the highs and lows experienced in Turkey since Endeavor launched in the country.

Digitization and AI Are Now Prerequisites

In emerging economies, digital transformation is no longer a luxury, but a prerequisite for growth. Technological innovation has created a basket of opportunities for existing business models to be disrupted and/or new business models to emerge. As a sector agnostic fund, we have direct exposure to these diverse and dynamic companies. (See Figure 13 below.) Automation and digitization have accelerated across industries as users become more tech-savvy and require more tailored solutions for their needs.

Though venture funding was down significantly in 2023, AI was a bright spot, trending higher year-over-year. Notably, AI is not specific to a particular industry and is not a discrete sector in and of itself; it’s a set of technologies that can be applied across very different companies, like Instadeep (Tunisia), a biotech AI company, NotCo (Chile), a food AI company, and AlcatrazAI (Bulgaria), a software AI company.

In the years ahead, we believe AI will move beyond the hype and focus on utility and efficiency as the reality of the technology sets in. Companies are now facing the realities of successfully deploying AI, including complex data management and the high cost of computing resources, forcing many to focus on viable business models.

Reid Hoffman (Partner, Greylock; Co-Founder of LinkedIn, Board Member, Endeavor Global) speaking at our 2023 Endeavor Catalyst Investor Meeting about the future of AI.

Fintech remains the most active industry in our portfolio, attracting 31% of our investment dollars in 2023. The boom of embedded finance, which allows companies in non-financial sectors to offer financial services to their customers without having to build a financial infrastructure from scratch, has paved the way for innovation and investment in the space.

We also believe digital assets and tokens will become safer and more mainstream with greater regulatory clarity and Wall Street participation. We are seeing the tokenization of real-world assets, such as commodities, currencies, and equities, which Bank of America anticipates being a key driver of digital asset adoption. The applications of Web3, particularly in emerging markets, are exciting and bode well for continued innovation and disruption in the financial sector globally.

We are seeing continued growth in frontier industries such as space, greentech, and biotech—each capitalizing on sector and/or geographic tailwinds. In Asia for example, we expect interest and investment in greentech (including agriculture and aquaculture) to continue to grow, with nine out of 10 ASEAN members making a strong commitment to achieving net-zero emissions by 2050.

Endeavor Catalyst has a unique perspective into the waves of technological innovation in each of our markets. In the chart below you can see how many investments we have made in each industry by region. (See Figure 14 below.)

We also believe digital assets and tokens will become safer and more mainstream with greater regulatory clarity and Wall Street participation. We are seeing the tokenization of real-world assets, such as commodities, currencies, and equities, which Bank of America anticipates being a key driver of digital asset adoption. The applications of Web3, particularly in emerging markets, are exciting and bode well for continued innovation and disruption in the financial sector globally.

We are seeing continued growth in frontier industries such as space, greentech, and biotech—each capitalizing on sector and/or geographic tailwinds. In Asia for example, we expect interest and investment in greentech (including agriculture and aquaculture) to continue to grow, with nine out of 10 ASEAN members making a strong commitment to achieving net-zero emissions by 2050.

Endeavor Catalyst has a unique perspective into the waves of technological innovation in each of our markets. In the chart below you can see how many investments we have made in each industry by region. (See Figure 14 below.)

Windows of Liquidity That Open and Shut

After a surge of liquidity in 2021/2022, 2023 ushered in a correction. The IPO and SPAC boom of 2021 created a new class of public companies that were not quite ready to be in the public eye. These zombie companies, unprofitable businesses that stay afloat by taking on new debt, make up 11.5% of US stocks and are underperforming market expectations. In this continued high-interest rate environment, we expect to see an increasing number of companies filing for bankruptcy or Chapter 11, as well as a greater number of take-private transactions. For some companies, filing for Chapter 11 or a take-private scenario can yield a second chance to grow more sustainably.

With underwhelming IPO performance, it’s no wonder the public markets in 2023 were only selectively open for companies with strong growth and profitability and/or a clear path to profitability. Many pre-IPO companies, including those in our own portfolio, postponed their plans to go public, holding out for more favorable market conditions.

Figure 15: Our Liquidity Over Time

The need for liquidity and lack of stability in public markets has contributed to an increase in cross-border M&A, which has been our primary source of liquidity over the past 10+ years. We believe well-capitalized companies will continue making acquisitions in their core businesses as they seek to gain market share and consolidate their positions as the industry leaders. We’ve seen this play out across Africa and Asia’s growth stage startups, particularly in overcrowded sectors such as fintech, B2B ecommerce, and logistics. This is an important step toward strengthening entrepreneurial ecosystems and offering better global solutions. Financial sponsors, such as PE firms, are also holding record amounts of capital and making acquisitions, leveraging the current opportunity to acquire startups at discounted prices.

Despite the challenging fundraising environment, the best companies are still prevailing. This year, we realized two exits: InstaDeep, an AI decision-making company out of Tunisia, was acquired for $650+ million by BioNTech, and GOintegro, an employee experience platform out of Argentina, was acquired by Edenred.

Windows of liquidity are not new to the venture asset class, and navigating the liquidity crunches in between them is key to the longtime survival of startups and venture capital firms alike.

The 300+ Companies in our Portfolio

Behind the 300+ companies in our portfolio are 380+ high-impact entrepreneurs dreaming big. They are transforming lives and economies across multiple industries worldwide. Learn more below!